How to Set Up a Business Bank Account in the UK

How to Set Up a Business Bank Account in the UK – Before you can even think about opening a business bank account, it’s critical to understand why it’s so important. This isn’t just another box to tick on your startup checklist; it’s a foundational move that separates your personal life from your business finances, makes tax time infinitely less painful, and builds a professional image from the get-go.

Why Your Business Needs Its Own Bank Account

Trying to run your business out of your personal current account is a recipe for disaster. It’s an administrative nightmare that creates confusion and can even cost you money. Setting up a dedicated business account is one of the first real steps you take to establish your venture as a serious, professional entity. This isn’t just about playing by the rules; it’s about giving yourself a clear financial picture to make smarter decisions.

This separation is absolutely vital for clean bookkeeping. When tax season rolls around, you’ll be patting yourself on the back for having a tidy record of every single business-related transaction. Imagine trying to justify a Tesco receipt mixed in with your software subscription payments to HMRC—a separate account just wipes that problem off the table. As an actionable insight, at the end of each month, you can download one simple bank statement that shows all your income and expenditure, ready for your accountant or bookkeeping software.

High-Street Banks vs. Digital Challengers

The bank you choose will have a real impact on your day-to-day operations. There’s no one-size-fits-all answer here.

A local retail shop owner, for example, will likely find a traditional high-street bank far more practical. They need a physical branch just around the corner to securely deposit cash takings every day and get face-to-face support when they need it. This becomes an actionable habit: at the end of each business day, they can walk to the bank and deposit the day’s cash, reducing risk.

On the flip side, a freelance digital marketer would probably be much better off with a modern, app-based bank. Their priorities are completely different: low fees for receiving payments from international clients and slick integration with accounting software like Xero or QuickBooks to automate their financial admin. For them, an actionable insight is to set up a ‘pot’ or ‘space’ within their digital account to automatically set aside a percentage of every incoming payment for their tax bill.

“Treating your business like a business from day one is non-negotiable. A separate account isn’t just good practice—it’s the bedrock of financial clarity and professionalism.”

This choice has become even more important in the UK’s bustling small business scene. In a market where 99.9% of registered businesses are SMEs, the banking options have had to adapt. Traditional high-street banks can sometimes have stricter criteria, asking for trading history or a minimum turnover, which can be a real hurdle for a brand-new sole trader.

In contrast, digital challenger banks have thrown the doors open, making business banking far more accessible for freelancers and micro-businesses with their straightforward, flexible sign-up processes. You can find out more about the UK business landscape from the British Business Bank.

Building Credibility and Financial Health

Beyond just keeping things organised, a business bank account is a powerful tool for building trust. When you send an invoice to a client, asking them to pay into an account with your business’s name looks infinitely more professional than one in your personal name. It sends a clear signal: you’re a legitimate, established operation.

This professional sheen has real, long-term benefits:

- Easier Access to Funding: When the time comes to apply for a business loan or overdraft, lenders will demand a clear financial history. A dedicated account provides that transparent record of your income and outgoings.

- Simplified Payments: It opens the door to accepting card payments and integrating with other professional payment systems.

- Clear Financial Tracking: You get a real-time view of your business’s financial health, which is essential for managing cash flow and budgeting effectively.

Ultimately, opening a business bank account is a strategic decision. It’s an investment in your company’s financial stability and future growth, right from the very beginning.

How to Choose the Right Bank for Your Business

Picking the right bank is about much more than just finding the lowest monthly fee. It’s about finding a financial partner that genuinely gets how your business works and can support you as you grow. This decision impacts everything, from your day-to-day transactions to your ability to grab funding when a big opportunity comes along.

Think about it: a construction firm will have completely different priorities from a tech startup. The builders will need robust credit facilities and face-to-face branch support to handle hefty, complex payments. The tech firm? They’ll be looking for slick API access to automate their finances and seamless integration with their accounting software to keep their lean operation humming.

Evaluating Your Core Banking Needs

Before you even start looking at comparison sites, take a moment to map out what your business’s financial life actually looks like. Getting this clear in your own head is vital because it separates the “must-haves” from the “nice-to-haves.”

Ask yourself a few key questions:

- Transaction Volume and Type: Are you expecting dozens of small online payments every day, or just a couple of large invoices each month? Will you be dealing with international clients and suppliers?

- Cash Handling: Is cash a big part of your business? If you’re running a café, a market stall, or a retail shop, being able to pop down to a local branch to deposit takings is non-negotiable.

- Credit Requirements: Do you anticipate needing an overdraft to smooth out cash flow bumps? Or perhaps a business loan down the line to invest in new equipment?

- Digital Tools: How important is a top-notch mobile app? Do you need multi-user access for your team or direct feeds into your bookkeeping software like Xero or QuickBooks?

Once you have the answers, you’ll have a solid checklist to measure each bank against.

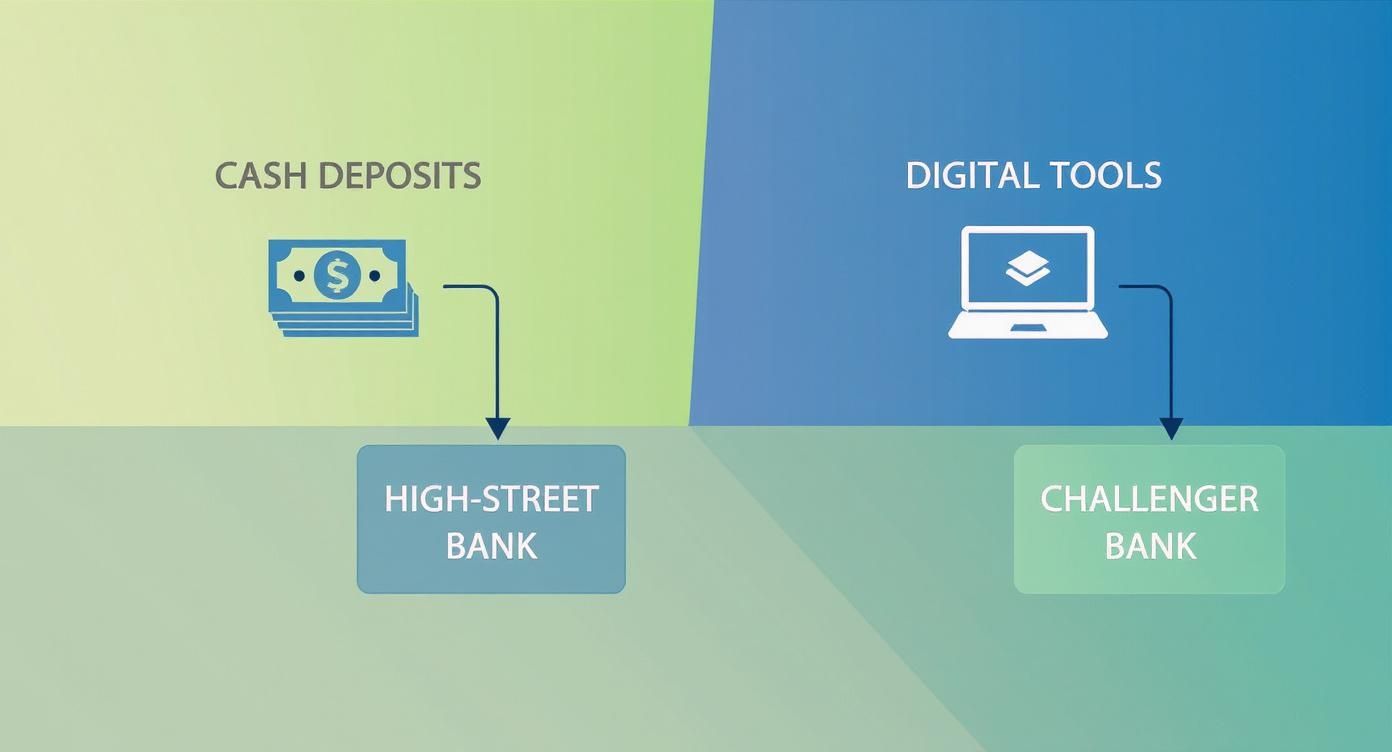

This decision tree gives a good visual breakdown of whether a traditional high-street bank or a newer challenger bank might be a better fit.

As you can see, businesses that rely on cash and in-person services are often better served by the established players. On the other hand, if digital efficiency is your top priority, a modern challenger bank could be the perfect match.

Traditional vs. Challenger Banks: A Quick Comparison

To help you weigh your options, here’s a look at how traditional high-street banks and modern digital challengers typically stack up against each other.

Comparing Key Features of UK Business Banks

| Feature | Traditional High-Street Banks | Digital Challenger Banks |

|---|---|---|

| Branch Access | Extensive network for in-person deposits, withdrawals, and advice. | Digital-only; no physical branches. All support is online or via app. |

| Account Opening | Can be slower, often requiring an in-person appointment and more paperwork. | Fast and entirely online, often taking just minutes to get an account number. |

| Digital Tools | Mobile apps are improving but can sometimes feel clunky or less intuitive. | Sleek, user-friendly apps with real-time notifications and advanced features. |

| Integration | Often have good integration with major accounting software, but API access can be limited. | Built around open banking with strong APIs for seamless software integration. |

| Lending Products | Offer a full suite of established products: loans, overdrafts, credit cards, mortgages. | Lending options can be more limited, often focused on smaller, shorter-term credit. |

| International Payments | Reliable but can be slower and more expensive with less transparent fees. | Typically faster and cheaper with transparent, real-time exchange rates. |

| Customer Support | Access to a dedicated relationship manager (for larger businesses) and branch staff. | Support is usually via in-app chat, email, or sometimes phone. |

This table isn’t exhaustive, but it highlights the core differences. Your “best” choice really depends on which of these columns aligns most closely with the needs you identified earlier.

The Growing Importance of Digital Features

There’s no denying the shift towards digital banking. In the UK, a huge 70% of business leaders now say they’d be happy using a bank with no physical branches at all. This trend is all about the convenience and efficiency that online-only providers deliver.

Choosing a bank is a long-term decision. Try to look past the flashy introductory offers and focus on the features that will genuinely save you time and support your growth. A good banking relationship should make your financial admin simpler, freeing you up to focus on what you do best: running your business.

Ultimately, the best bank is the one that fits your business model like a glove. For many startups and small businesses, a hybrid approach—perhaps a high-street bank for cash handling and a challenger for daily transactions—might even be the ideal solution. The key is to look beyond the headline fees and really dig into how an account’s features will work with your day-to-day operations.

For a deeper dive into structuring your company’s finances, take a look at our complete guide on business banking solutions.

Gathering Your Documents for a Smooth Application

Here’s a piece of advice that will save you a world of headaches: get your paperwork in order before you even think about starting an application. This isn’t just about ticking boxes. Banks are legally required to run strict “Know Your Customer” (KYC) and anti-money laundering checks, and a messy application is the quickest way to get stuck in limbo.

A practical tip: create a dedicated folder on your computer (or a physical one) and save digital copies of every required document. This makes uploading them quick and ensures you have everything in one place. Think of it as laying the groundwork for a solid banking relationship.

What Limited Companies Need

If you’re running a limited company, the bank needs to verify two things: the business itself and the people in charge. It’s a thorough process, but perfectly manageable if you have everything to hand.

You’ll need to pull together:

- Your Companies House registration number: This is your company’s unique ID.

- Certificate of Incorporation: The official document that proves your company legally exists.

- Proof of your trading address: A business utility bill or your office lease agreement works perfectly.

- Personal details for all directors: Full names, dates of birth, and home addresses covering the last three years.

- Details for Persons with Significant Control (PSCs): Banks must identify anyone owning 25% or more of the shares or voting rights. They’ll need proof of ID and address for these individuals, too.

Having this ready is a huge time-saver. It allows the bank to quickly cross-reference your details with the official Companies House records.

Documents for Sole Traders and Partnerships

For sole traders, things are generally a bit more straightforward. Since you and your business are legally the same entity, there’s no Companies House registration to worry about. The bank’s checks will focus on verifying your personal identity and your right to trade under your business name. A practical example of a required document would be your Unique Taxpayer Reference (UTR) number from HMRC.

If you’re in a partnership, the bank will need to verify every partner. Much like the directors of a limited company, each partner will need to provide their personal identification documents. You will also likely need a copy of your Partnership Agreement.

The single most common reason for application delays is painfully simple: incomplete or incorrect documents. Double-check that names and addresses match exactly across everything you submit. A tiny discrepancy can send you right back to the start of the process.

Essential Personal Identification for Everyone

No matter your business type, every single person named on the account—director, partner, or sole trader—needs to prove who they are. Banks are very specific about this and typically ask for two key pieces of information.

- Proof of Identity: This must be a valid, government-issued photo ID. A passport or a UK driving licence is the standard. Crucially, make sure it’s in date!

- Proof of Address: You’ll need a recent document (usually from the last three months) that clearly shows your current home address. A utility bill, council tax statement, or a personal bank statement are the most common options.

Recent regulations have tightened up these requirements, and you can learn more about how UK company directors must prove their identity in our guide. Ensuring these documents are clear, current, and easy to read is the best thing you can do to help your application fly through without a hitch.

Navigating the Bank Application Process

Once you have your documents in order, it’s time to get down to the application itself. This is the part where your business starts to feel real, at least in the eyes of the bank. Getting the details right here is absolutely critical to avoid unnecessary delays.

Whether you’re applying online from your sofa or heading into a branch for a face-to-face chat, the information you’ll need to provide is pretty much the same. The application form will dig deeper than just your name and address; it’s designed to build a clear and accurate picture of your new venture.

Filling Out the Key Application Sections

You’ll come across a few specific questions that help the bank understand your business’s financial pulse. It pays to take your time here, as thoughtful, consistent answers will make the whole process much smoother.

- Projected Annual Turnover: This is simply your best guess at how much money your business will bring in during its first year. Be realistic. A freelance copywriter just starting out might project £25,000, based on securing two clients a month at an average project fee. An e-commerce store might project £70,000 based on selling 20 units per day. Banks use this to get a feel for the size of your operation.

- Business Activities: Vague answers won’t cut it. Instead of just putting “IT services,” try something like “providing remote IT support and cybersecurity consultancy for small UK businesses.” The more specific you are, the better the bank can understand your industry and any associated risks.

- Expected Transactions: The form will probably ask about the volume and type of payments you expect. For instance, a coffee shop might anticipate 500+ incoming card payments per week and 5-10 outgoing payments to suppliers. Crucially, if you have any plans to trade internationally, you need to state that upfront.

Being straight and clear on these points helps the bank meet its regulatory obligations and ensures they set you up with an account that’s actually fit for purpose.

The Online Application Journey

For most new entrepreneurs, applying online is the quickest and easiest route. It’s convenient and can usually be done and dusted in a single session. The grand finale is almost always the identity verification.

This part is usually quite a slick, app-based procedure:

- You’ll be asked to snap a clear photo of your passport or driving licence.

- Then, you’ll record a short video of yourself, sometimes repeating a phrase or turning your head from side to side.

- Some clever tech then matches your face to your ID, confirming who you are in just a few minutes.

A classic mistake is providing slightly different information across your documents. Make sure the business address on your application form is an exact match for the one on your Companies House registration or utility bills. The smallest discrepancy can flag your application for a manual review, slowing everything down.

Preparing for an In-Branch Appointment

If you’re going with a more traditional high-street bank or your business structure is a bit more complex (like a partnership), you might need an in-branch appointment. Don’t see this as a hurdle; it’s a brilliant opportunity to start building a relationship with your bank manager.

Think of it as a friendly, informal chat about your business. The advisor will want to hear about your business model, who your customers are, and what your ambitions are. An actionable tip: prepare a one-page summary of your business, including your mission, target customer, and projected turnover. This shows you are organised and serious.

Managing Your New Business Account Effectively

The approval is in and your account number is official—congratulations! It’s a genuine milestone, but the real work starts now. Getting your new business bank account up and running properly from day one will save you countless hours down the line.

Your first practical steps are straightforward but absolutely essential. You’ll need to formally activate the account, which might just be a final online confirmation or a quick phone call. At the same time, get your online and mobile banking portals set up and order your business debit card. Don’t put this off; you need these tools for daily operations.

Making Your Account Work for You

Once the basics are sorted, it’s time to move beyond simple transactions. Your account should be an active part of your financial toolkit, not just a place to hold cash. Modern business accounts come packed with features designed to simplify your admin.

For instance, identify all your recurring business expenses—software subscriptions, rent, or supplier retainers—and set up standing orders immediately. This simple act of automation prevents missed payments and helps you maintain a predictable cash flow. For a small business, predictable outgoings are a huge advantage.

Another powerful move is to connect your bank account directly to your accounting software. Most banks now offer a direct feed into platforms like Xero or QuickBooks. This connection automatically pulls in your transaction data, drastically cutting down the manual slog of bookkeeping.

Setting up these automated connections isn’t just about convenience; it’s about maintaining accuracy. The less manual data entry you do, the lower your risk of costly errors when it’s time for your tax return.

Many digital banks also offer brilliant built-in tools. Keep an eye out for features like spending categorisation, which can automatically tag your outgoings, or integrated invoicing tools that let you create and send professional invoices straight from your banking app. An actionable insight is to create a ‘rule’ that automatically allocates all payments from a specific client to your ‘Income’ category.

Protecting Your Business Funds

As soon as your account is active, so is your responsibility to keep it secure. Business accounts are a prime target for fraudsters, so implementing robust security measures is non-negotiable.

- Enable Two-Factor Authentication (2FA): This adds a crucial layer of security, requiring a second step (usually a code sent to your phone) before anyone can log in.

- Be Vigilant Against Phishing: Never click on suspicious links in emails claiming to be from your bank. Always log in directly through the official website or app.

- Set Up Transaction Alerts: Configure notifications for payments going in or out of your account. This gives you a real-time view of all activity and flags anything unexpected instantly.

Properly managing your account is just as important as knowing the importance of keeping accurate accounts for your business’s long-term health. By activating key features and prioritising security from the start, you can transform your new account from a simple place to hold money into a powerful business management tool.

Got a Few More Questions About Business Bank Accounts?

Even with the clearest plan, a few niggling questions can pop up when you’re setting up a business bank account. Let’s tackle some of the most common queries we hear from UK entrepreneurs, giving you the straightforward answers you need to get this sorted.

Can I Open a UK Business Bank Account if I’m Not a Resident?

Opening a UK business account when you don’t live here can be tricky, but it’s definitely not impossible. While most high-street banks will want at least one director to be a UK resident, the game is changing.

Many of the newer, digital-first banks and financial specialists are far more flexible, particularly if your company is officially registered in the UK with Companies House. Just be ready for a more thorough verification process. You’ll almost certainly need to provide internationally recognised proof of ID and address from your home country. The best advice? Always check the specific eligibility criteria on a bank’s website before you dive into an application.

How Long Does It Take to Open a Business Bank Account?

This is a real “how long is a piece of string?” question. The time it takes to get your shiny new account number can vary wildly. Digital challenger banks are built for speed—they can often approve applications and give you your account details within a few hours, provided all your documents are in order and your identity check sails through.

On the other hand, traditional high-street banks often have a longer, more formal process. You could be waiting anywhere from a few working days to a couple of weeks, especially if your application needs an in-branch appointment or if your business structure is a bit more complex.

Want to speed things up? Have all your key documents scanned and ready to upload before you start. Responding instantly to any follow-up emails from the bank also helps keep the momentum going.

Do I Legally Have to Get a Business Account as a Sole Trader?

This is a massive point of confusion for so many new business owners. The short answer is no. In the UK, it is not a strict legal requirement for a sole trader to have a separate business bank account. You can legally run your business finances through your personal current account.

But just because you can, doesn’t mean you should.

It is highly, highly recommended you open a dedicated account. Why? Because it makes tracking your income and expenses for your annual Self Assessment tax return about a million times easier. It also avoids the messy and potentially awkward situation of mixing personal and business funds, which can raise eyebrows with HMRC.

Besides the practical stuff, it just looks far more professional to your clients. Many banks now offer specific accounts for sole traders with low or even zero monthly fees, making the decision to keep your finances separate a total no-brainer.

Setting up the right foundations for your business goes beyond just banking. At Acorn Business Solutions, we provide a full suite of services—from company formation and virtual office addresses to compliance support—designed to help UK entrepreneurs start and grow with confidence. Find out how we can help you.

Related Topics

What Is a Memorandum and Articles of Association

What is a memorandum and articles of association? This guide breaks down these key UK company documents with clear examples for founders and startups.

A Guide to the Companies House Certificate of Good Standing

What is a Companies House Certificate of Good Standing? Learn why your UK business needs one, when to get it, and the step-by-step process to apply.

How to Write a Business Plan UK That Secures Funding

Learn how to write a business plan UK with our guide. Get actionable insights, real-world examples, and proven templates to turn your vision into reality.

8 Key Advantages of Being a Limited Company in the UK for 2026

Discover the top advantages of being a limited company. Our guide covers liability, tax efficiency, and credibility to help you decide if it’s right for you.

Professional Indemnity Insurance

Discover what is professional indemnity insurance, why your business needs it, and how it shields you from costly client claims.

What is a company secretary

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,