Business Bank Account for Non UK Resident

Business Bank Account for Non UK Resident – It’s a common question we get: can I open a UK business bank account if I don’t live in the UK? The short answer is yes, absolutely. But you need to go about it the right way.

For nearly every international founder, the journey begins with one crucial, non-negotiable step: forming a UK limited company. This creates the official legal entity that UK banks—whether they’re high-street giants or slick digital challengers—need for their compliance checks.

Your Roadmap to a UK Business Bank Account

Expanding into the UK is an exciting prospect, but navigating the financial system can feel like a maze. Many entrepreneurs are surprised to find they can’t just open an account for their existing overseas company. Instead, getting a business bank account for a non-UK resident almost always starts by establishing a proper UK footprint.

Think of it from the bank’s perspective. They need to verify that the business they’re dealing with is a recognised UK entity, registered with Companies House. This isn’t just red tape; it’s a legal requirement to meet strict anti-money laundering (AML) and Know Your Customer (KYC) regulations. Without a UK-registered company, your application will be a non-starter.

The Two Paths to UK Banking

Once your UK company is set up, you have two main routes to choose from:

- Traditional High-Street Banks: We’re talking about the big names like Barclays or HSBC. While they offer credibility, they often throw up roadblocks for non-residents. Expect strict requirements for a UK residential address for directors and, in many cases, a mandatory in-person branch visit. For example, you might complete an online form only to be told the final step is a face-to-face meeting in London.

- Digital Providers and Fintechs: Modern financial platforms like Wise or Revolut were built for a global audience. Their application processes are usually fully remote, they’re more flexible with international documents, and you could have an account approved in days, not weeks.

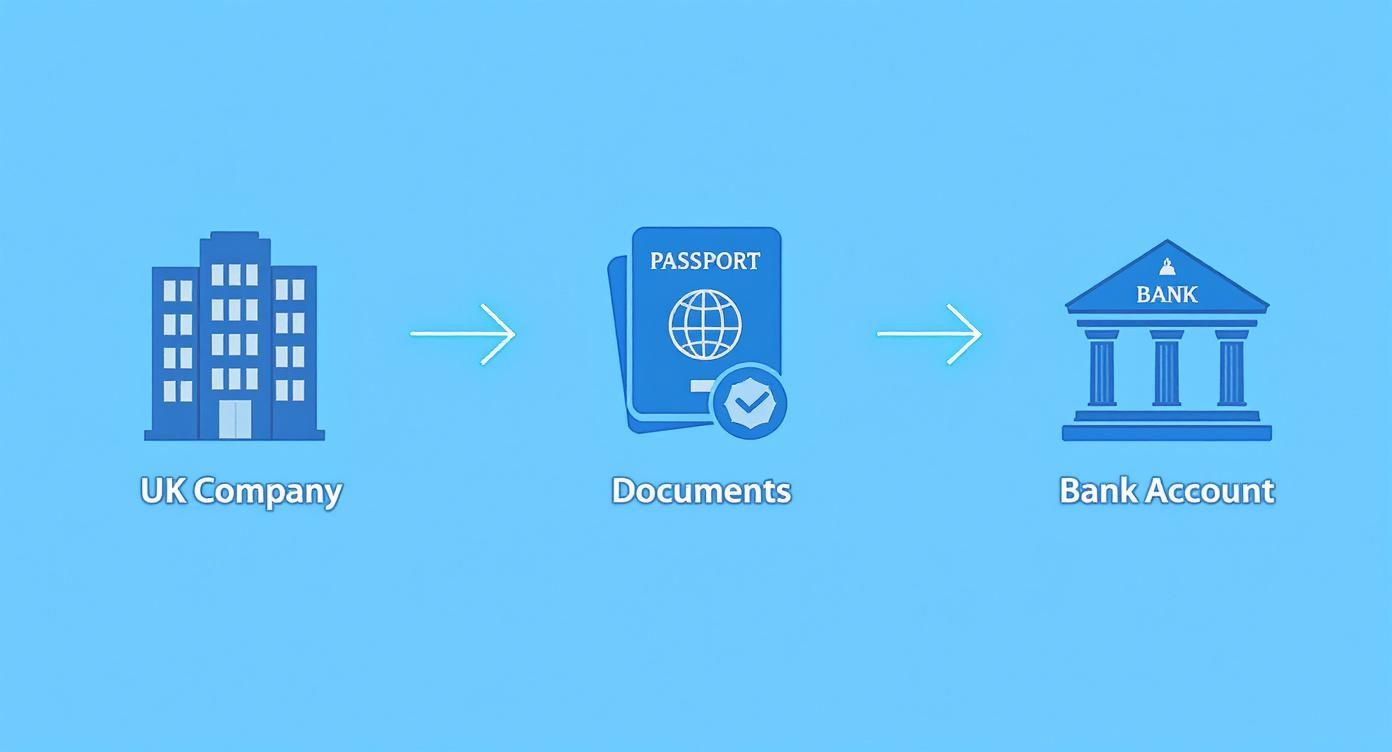

This flowchart breaks down the essential steps for any non-resident looking to secure a UK bank account.

As you can see, forming a UK company is the foundation you build everything else on. For most international founders, going with a digital provider is the path of least resistance. It’s faster, more accessible, and helps you sidestep the common hurdles thrown up by traditional banks.

The core challenge isn’t your residency status itself, but proving to the bank that your UK-registered business is legitimate and compliant. Forming a company is the first and most important piece of that puzzle.

So, while opening a UK business bank account as a non-resident has its complexities, it’s entirely doable. The process starts with registering your limited company. To do that, you’ll need a certificate of incorporation from Companies House, a company registration number (CRN), a UK-registered business address, and proof of your identity (like a passport).

This guide will walk you through each stage, giving you the practical insights you need to get it done.

Establishing Your UK Company From Abroad

Before you can even get in the door with a UK bank, you need to lay the proper legal groundwork. This means forming a UK limited company. It’s the first, non-negotiable step that officially puts your business on the map with Companies House, the UK’s official registrar.

Think of it this way: for a UK bank, a registered limited company is proof of legitimacy. It’s a recognised legal entity they can verify, which is absolutely essential for their anti-money laundering (AML) and Know Your Customer (KYC) checks. Without it, your application for a business bank account as a non UK resident will be a non-starter.

Choosing a Unique Company Name

Your first practical task is picking a name for your company. It has to be unique and not already taken on the Companies House register. A quick search on their online database is the best way to see if your preferred name is free.

There are a few rules to follow. Your name can’t be offensive or pretend to have a connection with the government unless you get specific permission. It also can’t be almost identical to an existing name. For example, if “Innovate Solutions UK Ltd” is already registered, you won’t be able to register “Innovate Solution UK Ltd.” An actionable tip is to check the availability of a matching domain name at the same time to ensure your online branding can be consistent.

Appointing Directors and Shareholders

Here’s some good news for international founders: there is no requirement for company directors to be UK residents. You can appoint yourself and other key people from anywhere in the world. You’ll just need to provide some basic personal details for each director, which will be available to the public on the Companies House register.

Next, you need to sort out your company’s share structure. For most new businesses, this is incredibly straightforward:

- Shareholders: You need at least one shareholder. This person can also be the director.

- Shares: A very common setup is to issue a single share worth £1.00. This keeps everything wonderfully simple.

This structure defines who owns the company and is a critical piece of information you’ll need during the formation process. If you want to dive deeper into the nuts and bolts, our guide on UK company formation for non-residents covers everything in detail.

Solving the UK Address Requirement

Now we come to the biggest hurdle most non-residents face: every UK limited company legally must have a UK address. This isn’t optional, but it definitely doesn’t mean you need to rent a physical office. In fact, you’ll need two different types of addresses.

The key to operating from abroad is understanding the difference between a Registered Office Address and a Director’s Service Address. Using specialised services for these is not just allowed; it’s the standard, cost-effective solution for international entrepreneurs.

A Registered Office Address is your company’s official, public-facing address. All statutory mail from Companies House and HMRC gets sent here. It must be a physical UK address, not a PO Box.

A Director’s Service Address is the official correspondence address for each director. This address also goes on the public record. You could use your home address, but that means it will be publicly visible to anyone who looks up your company. A practical insight is to use a service address to protect your personal privacy.

The smart, practical solution is to use a virtual office or mail forwarding service. These services give you a professional and fully compliant UK address for both your registered office and your directors’ service needs. It’s an essential service that makes the whole process of setting up a UK company from abroad both feasible and affordable.

Getting Your Paperwork in Order

Once your UK company is officially formed, the next hurdle is pulling together a flawless set of documents. Honestly, a successful application for a business bank account for a non UK resident often hinges on the quality of your paperwork. Getting this right from the start saves a lot of back-and-forth and shows the bank you’re a serious, organised applicant.

Banks are under a legal microscope to verify exactly who they’re doing business with. This means every document you submit must be clear, current, and perfectly consistent. Even a tiny discrepancy, like a slight name variation between your passport and a utility bill, can raise red flags and grind the whole process to a halt.

Essential Personal ID

First up, every director and major shareholder (that’s usually anyone who owns 25% or more of the company) needs to provide personal identification. This is a non-negotiable part of the Know Your Customer (KYC) checks.

- Valid Government-Issued Photo ID: Your passport is the gold standard here. It’s universally recognised and designed for international verification. An actionable tip: check your passport’s expiry date. If it’s due to expire within six months, renew it before you start your application.

- Proof of Personal Address: This is often the biggest stumbling block for non-residents. Banks need to see a recent, official document that ties you to your residential address in your home country. Crucially, it must be dated within the last three months. A practical example would be a PDF of your electricity bill from last month showing your name and full address.

The best options are usually a utility bill (electricity, water, gas), a bank statement from a personal account, or an official tax document. A word of warning: mobile phone bills are almost always rejected, so stick to more established forms of proof. While you might be looking into a virtual address for business in the UK for your company’s mail, remember this is completely separate from your personal proof of address.

Company and Business Documents

Next, you’ll need the official records for your newly minted UK limited company. These documents are the proof of its legal existence and structure. The good news is that these are easy to get your hands on once you’ve registered with Companies House.

You’ll may be asked for:

- Certificate of Incorporation: Think of this as your company’s birth certificate. It shows the name, formation date, and the all-important company registration number (CRN).

- Memorandum and Articles of Association: These documents lay out the company’s purpose and the internal rulebook for how it will be run, covering everything from directors’ responsibilities to shareholder rights.

A common slip-up is assuming digital copies will always do. While most fintech providers are happy with high-quality scans, always double-check. More traditional high-street banks might insist on certified copies or even original documents.

Dealing with Documents Not in English

If any of your key documents—like your proof of address or ID—are not in English, you’re going to need a professional translation. Banks won’t accept a version you’ve translated yourself or one done by a friend.

You must use a certified translator who will provide a signed statement confirming the translation is accurate. This adds an extra step and cost, so it’s smart to figure out which documents need translating early on. For example, if your bank statement is in Spanish, you’ll need a translated copy alongside the original. Some banks might even require the translation to be notarised, so it pays to confirm their specific rules before you start.

The High-Street Bank Hurdle

We’ve all heard of the big names—HSBC, Barclays, Lloyds. They carry the weight of history and reputation, and for a UK local, they’re the obvious choice. For a non-resident director, however, their processes can feel like they were designed in a different century.

The biggest showstopper is almost always the demand for an in-person branch visit. If you’re running your business from another country, that’s an immediate and expensive deal-breaker. Even if you can make the trip, you’ll likely hit another wall: the rigid insistence on proof of a UK residential address for directors, which most international founders simply don’t have.

On top of that, their processing times for international applications are notoriously slow. We’re talking anywhere from four weeks to several months, often with confusing back-and-forth requests for more documents. While their brand name is solid, the reality for a non-resident is a high-friction process with a low chance of success.

The Digital Provider Advantage

This is where the financial technology (fintech) providers come in. They were born out of a need for more accessible, global banking, so their entire model is built around the remote, digital world you operate in.

Their biggest plus? The application is 100% remote. You can do everything from your laptop or phone, wherever you are. Identity verification is handled smartly and digitally—usually by uploading a photo of your passport and taking a live selfie or a short video. It’s quick and secure.

These providers are also far more switched-on when it comes to documents. They’re used to seeing international proof of address from your home country and have systems designed to verify them quickly. This flexibility often extends to clearer fee structures and, most importantly, much faster turnaround times. It’s not uncommon for applicants to get their accounts approved in as little as 24 to 72 hours. Our complete guide on how to set up a business bank account dives deeper into what you can expect from these modern platforms.

For the vast majority of non-resident founders, the path of least resistance and highest success runs directly through a digital-first provider. Their systems are designed for your exact situation, removing the geographical barriers that traditional banks impose.

To lay it all out, let’s compare the two options side-by-side.

Traditional Banks vs Digital Providers for Non-UK Residents

Choosing between a high-street institution and a digital provider is one of the most important decisions you’ll make when setting up your UK company from abroad. This table breaks down the key differences you’ll encounter.

| Feature | Traditional High-Street Banks | Digital/Fintech Providers |

|---|---|---|

| Application Process | Often requires an in-person branch visit in the UK. | 100% online and remote, from anywhere in the world. |

| ID Verification | Manual checks in-branch, strict document requirements. | Digital verification using passport scans and live selfies or video. |

| Proof of Address | Rigid rules; may insist on UK residential proof for directors. | Flexible; readily accept utility bills or bank statements from your home country. |

| Account Opening Speed | Slow, typically taking 4-12 weeks or even longer. | Fast, with accounts often approved within 1-3 business days. |

| Account Features | Full suite of services including loans and overdrafts. | Focused on core banking, multi-currency wallets, and international payments. |

| Ideal User | UK-resident directors or companies with a significant physical UK presence. | Non-resident directors, e-commerce businesses, and digital service providers. |

Ultimately, while the name recognition of a high-street bank might seem appealing, a digital provider offers a far more practical and efficient solution for opening a business bank account as a non UK resident. They understand the unique challenges you face and have built their services to solve them, letting you get your banking sorted quickly so you can focus on what really matters—growing your company.

Getting Through the Application and Verification Maze

Alright, you’ve got your documents in order and you’ve picked your banking partner. Now for the final hurdle: the application itself. This stage is all about proving your business is legitimate and sailing through the bank’s verification checks. For a non-resident, this is your moment to show you’re a credible, low-risk client they’ll want to work with.

Most modern banking applications are refreshingly simple and can be done online in less than an hour. Don’t let that fool you into rushing, though. An actionable tip is to complete the application on a desktop computer where you have all your document files ready in a single folder, making uploads quick and easy.

Making Your Business Case Crystal Clear

When you’re filling out the application form, you need to paint a clear, coherent picture of your company. Think of it as answering a compliance officer’s questions before they even have to ask them.

- Business Activities: Get specific. Don’t just put “e-commerce.” A much better example is, “selling artisanal, handcrafted leather goods online to UK and EU customers.” If you’re in services, go with “providing SEO consulting services to UK-based tech start-ups.”

- Source of Funds: Be upfront about where the money is coming from. A simple explanation like “funded through personal savings from my career as a software engineer” is far more effective than leaving it blank. If you have investors, be ready to name them.

- Projected Turnover: Give them a realistic number for your first year. This shows you have a proper business plan and helps the bank gauge your expected transaction volume. A projection of £50,000 for a new solo venture is far more believable than plucking a seven-figure sum out of thin air.

This section is essentially your business’s elevator pitch to the bank. A clear, logical summary makes their due diligence straightforward, which means a much faster approval for you.

The golden rule of any bank application is consistency. Every single detail, from your director’s middle name to your business description, must perfectly match what’s on your official documents and your Companies House registration. Mismatches are the number one reason applications get rejected.

Acing the Identity Checks (KYC & AML)

Once you hit ‘submit’, you’ll move into the Know Your Customer (KYC) and Anti-Money Laundering (AML) verification stage. For anyone applying for a business bank account non UK resident, this is now almost always a quick, digital process.

The most common method is a remote identity check. The bank’s app will ask you to take a high-quality photo of your passport. Then, you’ll usually be prompted to take a live selfie or record a short video of yourself, perhaps turning your head or saying a few words. This ‘liveness’ check confirms it’s really you, matching your face to your passport photo in real time.

Let’s walk through a real-world example:

Say you’re applying from Dubai. The app asks you to upload your passport. You take a clear picture, making sure there’s no glare and all four corners are visible. Next, it prompts you for a selfie. You find a room with good lighting, take off your sunglasses, and follow the on-screen instructions. The whole thing takes less than two minutes – a world away from having to fly to the UK for a face-to-face meeting.

This digital verification is incredibly secure and efficient, often giving you an answer within a few hours. By tackling this final step with care, you can secure your UK bank account smoothly and avoid the common traps that trip up so many international founders.

Common Questions from Non-Resident Founders

Setting up a UK business bank account from another country can feel like navigating a maze. It’s no surprise that we get a lot of questions from international founders. Let’s tackle some of the most common ones we hear.

Can I Really Open an Account Without Visiting the UK?

Yes, you absolutely can. If you’re used to traditional banking, the idea of opening an account without an in-person meeting might seem strange, but the financial world has changed. The trick is to pick the right provider.

Your typical high-street bank will almost certainly ask at least one director to pop into a UK branch for a face-to-face chat. For most international founders, that’s an immediate deal-breaker.

This is where digital providers and fintechs come in. Their entire model is built for remote, online applications. They use secure and sophisticated ID verification technology to meet their legal obligations, which usually involves you:

- Uploading a crisp, clear photo of your passport.

- Doing a quick “liveness” check, like taking a selfie or a short video of you turning your head.

This tech lets them complete their Know Your Customer (KYC) checks without you ever leaving your home office. It’s why digital providers are nearly always the best bet for opening a business bank account as a non-UK resident.

What Is a Registered Office Address and Is a Virtual One Okay?

Every UK limited company must have a registered office address. This is your company’s official, legal home—it’s not just a mailing address. It has to be a physical UK address where official bodies like Companies House and HMRC can send statutory mail. A simple PO Box just won’t cut it.

For non-resident directors, using a virtual office or a mail forwarding service is the standard, common-sense solution. It gives you a fully compliant UK address and ensures you meet your legal duties without the massive overhead of renting a physical office.

Key distinction: Your registered office is your company’s legal address. It is not your personal residential address. Banks will still need to see separate proof of where you live in your home country, like a recent utility bill or bank statement. Checkout our professional registered office address service

How Long Does the Account Opening Process Really Take?

This is where the path you choose makes a massive difference. We’re not talking a few days’ variation—it can be weeks or even months.

With a digital provider, the process is fast and slick. If you have all your documents ready to go, it’s not unusual to have your account approved and ready to use in 24 to 72 hours. A practical example is an entrepreneur in Singapore who formed their company on a Monday, applied for a digital bank account on Tuesday with all documents ready, and received their account details by Wednesday afternoon.

Trying your luck with a traditional high-street bank is a whole different story. Expect manual reviews, deeper checks on non-resident applicants, and back-and-forth requests for more information. Realistically, you could be waiting anywhere from four weeks to several months, and even then, there’s no guarantee they’ll approve you.

Does My Personal Credit History in My Home Country Matter?

This is a big worry for many founders, but it’s one you can usually set aside. When you apply for a UK business account, the bank isn’t running a credit check on you in your home country.

Their main focus is on two things:

- Verifying who you are to comply with strict anti-money laundering rules.

- Understanding your business and assessing its risk profile.

They want to know what your company does, where its money comes from, and who owns it. The checks are all about compliance and business legitimacy, not whether you paid your personal credit card on time back home.

Will My Application Be Rejected Because I Am a Non-Resident?

Being a non-resident doesn’t automatically get you rejected, but it does mean your application will get a closer look. When applications from international founders get turned down, it’s usually for specific, avoidable reasons.

Here are the most common tripwires we see:

- Inconsistent Details: Small differences between your application form and your documents, like a typo in your name or a slightly different address.

- Poor-Quality Documents: Sending blurry scans, photos of expired IDs, or a proof of address that’s older than three months.

- A Vague Business Description: If you can’t clearly explain what your business does, how it’s funded, and who your customers are, it raises red flags.

- Applying to the Wrong Bank: Wasting time applying to a traditional bank that has a firm policy against directors without a UK residential address.

You can dramatically boost your chances of a quick approval by picking a fintech that welcomes international customers and taking the time to get your documents perfectly in order.

Getting your UK company and its banking sorted from overseas might seem daunting, but it’s perfectly achievable with the right preparation. At Acorn Business Solutions, we specialise in providing the core services you need to get started, from UK company formation to virtual office addresses that give you a professional UK presence right away.

Explore how our services can simplify your UK expansion at https://acornbusinesssolutions.com.

Key Responsibilities at a Glance

Blog Categories

- Startups

- Sales & Marketing

- Leadership

- Finance & Accounting

- Technology & Innovation

- Customer Experience

- Sustainability & Ethics

- Personal Development

- Success Stories

- Legal & Compliance

- Hiring & HR

- Small Business Tips

- E-Commerce

- Networking

- Acorn Insights

- Industry News

Related Topics

Professional Indemnity Insurance

Discover what is professional indemnity insurance, why your business needs it, and how it shields you from costly client claims.

What is a company secretary

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

How Do You Redirect Your Mail in the UK?

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

Top accounting courses for small business in the UK (2025)

Discover accounting courses for small business in the UK. Compare top options, pricing, and formats

UK Business Bank Accounts With No credit Checks

Discover UK business bank accounts with no credit checks. This guide explains your options and eligibility

Managing cash flow for small business: Quick tips

Discover managing cash flow for small business with practical steps to forecast, optimize liquidity,