Professional Indemnity Insurance Guide

Professional indemnity insurance (PI) is your financial safety net if you’re a UK business or sole trader providing advice or professional services. It’s designed to protect you if a client ever claims your service was negligent or that a mistake you made cost them money. The policy covers your legal defence fees and any compensation you might have to pay.

Understanding Your Professional Safety Net

Think of professional indemnity insurance as a vital shield for your expertise. Whether you’re a management consultant, a web developer, or a graphic designer, you get paid for your knowledge and skills. But what happens if that advice, however well-intentioned, leads to a client suffering a financial loss?

Even if a claim against you is completely baseless, the cost of defending your business can be staggering. This is exactly where PI insurance steps in.

It’s not about admitting you did something wrong; it’s about having the resources to handle a dispute without it derailing your entire business. A single allegation of negligence can set off a chain reaction of legal consultations, court dates, and potentially huge settlement payments. For many small businesses and sole traders, those costs are simply impossible to bear. You can find out more about common pitfalls that leave new companies exposed by reading about the 5 mistakes that can tank your startup business.

To put it into perspective, let’s quickly summarise what PI insurance is all about.

Professional Indemnity Insurance At a Glance

This table breaks down the core purpose of Professional Indemnity (PI) insurance.

| Core Function | What It Covers | Who It’s For |

|---|---|---|

| Financial Protection | Legal defence costs, compensation payments, and settlement fees arising from claims of professional negligence, errors, or omissions. | Any UK business, freelancer, or contractor providing professional advice, design, or services. |

| Risk Management | Acts as a crucial buffer against the financial fallout from client disputes, allowing you to operate with confidence. | Consultants, accountants, architects, IT professionals, marketers, designers, and many other service-based roles. |

| Client Confidence | Often a contractual requirement, showing clients you are a professional who takes responsibility for your work seriously. | Professionals in industries where mistakes can have significant financial consequences for clients. |

Essentially, it’s a foundational element of responsible business management, ensuring one client dispute doesn’t undo all your hard work.

Why It Matters in the UK Market

The need for this kind of protection is huge right across the United Kingdom. With the rise of freelancers and service-based businesses, PI insurance has become a vital safeguard against claims of negligence or mistakes. The UK market for this cover is massive, with an estimated premium value of around £3.5 billion annually.

There are approximately 1.5 million policyholders nationwide, a number that continues to grow as more people go into business for themselves. You can discover more insights about the PI insurance market on ProfessionalIndemnity.co.uk.

This insurance provides more than just financial cover; it offers peace of mind. Knowing you have a policy in place allows you to focus on delivering high-quality services to your clients, confident that you are protected against unforeseen professional risks that could otherwise jeopardise your business’s future.

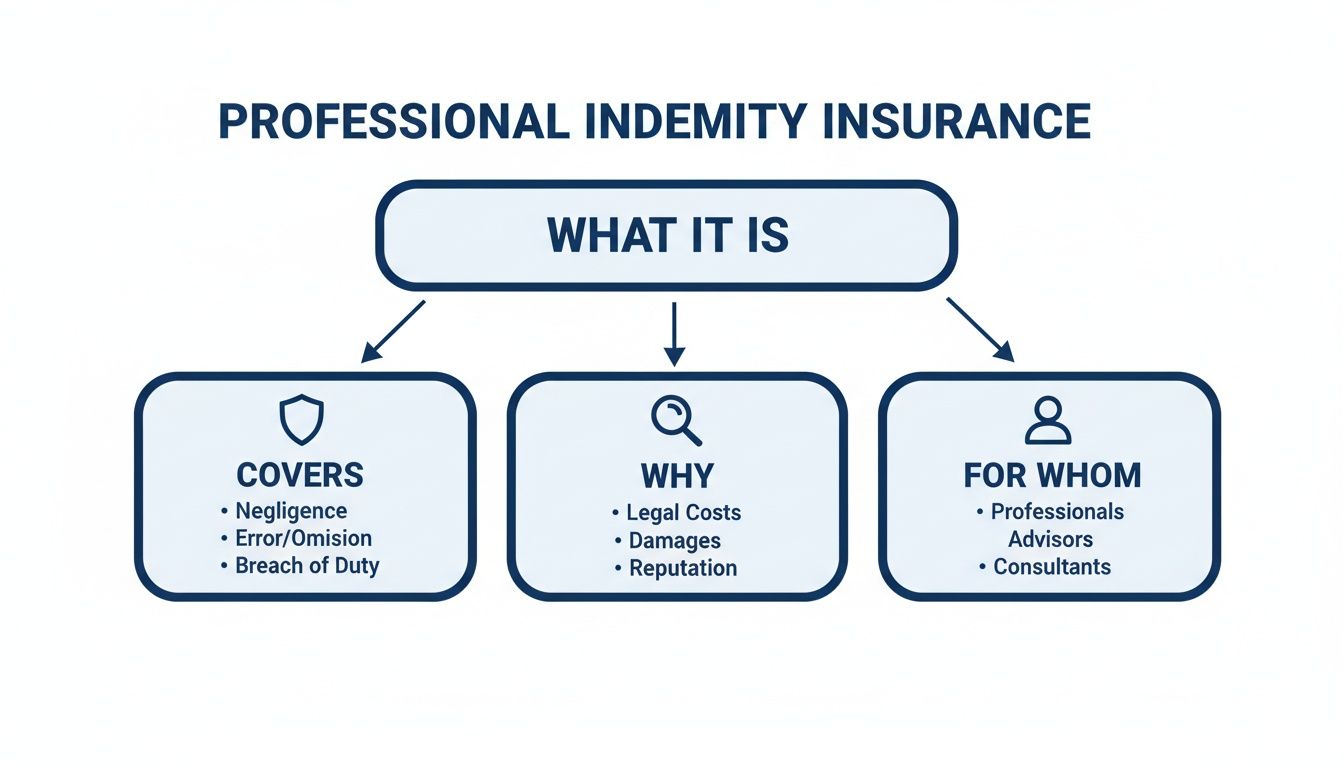

Who Actually Needs PI Insurance in the UK?

Figuring out whether you need professional indemnity (PI) insurance can feel a bit murky. Is it an absolute must-have, or just a nice-to-have safety net? The short answer is: it really depends on your profession, who your clients are, and the kind of risks that come with the services you provide. For most UK professionals, the need for this cover boils down to one of three situations.

This diagram gives a quick visual rundown of what professional indemnity insurance is all about, why it’s so important, and the kinds of businesses it’s designed for.

As you can see, the policy acts as a shield, mainly for professionals whose advice or services could, if things go wrong, lead to a dispute with a client. Let’s break down exactly who falls into that category.

Category 1: Required by Law or a Regulatory Body

For some UK professions, having PI insurance isn’t a choice—it’s a mandatory part of the deal if you want to practise legally. These roles are typically overseen by professional bodies that set minimum cover levels to protect the public from bad advice or mistakes. If you’re in one of these fields, you simply can’t offer your services without a valid policy.

This group includes roles where the stakes are particularly high:

- Solicitors and Accountants: Given the serious nature of financial and legal advice, bodies like the Solicitors Regulation Authority (SRA) and the Institute of Chartered Accountants in England and Wales (ICAEW) insist on it. PI insurance is non-negotiable for a huge range of professionals, including legal professionals and law firms, to guard against claims of negligence or errors.

- Architects and Surveyors: Professional bodies such as the Architects Registration Board (ARB) and the Royal Institution of Chartered Surveyors (RICS) require their members to have adequate cover.

- Financial Advisers: The Financial Conduct Authority (FCA) mandates that all regulated financial advisers must hold PI insurance to operate.

Category 2: Required by Your Clients

Next up are the professionals who might not be legally obliged to have PI insurance but find it’s practically impossible to win work without it. Here, it’s the clients who are driving the demand. This is especially true in the business-to-business world, where a client wants solid proof that you can cover any financial losses your work might cause them.

Actionable Insight: A potential client asking to see your PI insurance certificate is a great sign. It means they’re serious about managing risk and expect their suppliers to be just as professional. Not having cover can be an instant deal-breaker.

Think about an IT consultant pitching for a major corporate project. They will almost certainly find that PI insurance is a non-negotiable clause in the contract. Why? Because a single mistake, like a website bug that takes the client’s e-commerce site offline, could result in massive financial losses. The client needs to know you’ve got a policy in place to handle that kind of claim.

Category 3: Required for Smart Risk Management

Finally, there’s a huge and growing group of professionals who get PI insurance for one simple reason: it’s just good business sense. No regulator or client might be breathing down their neck, but they understand the real-world risks of offering a professional service. One mistake, one unhappy client, and they could be facing a claim that puts their business—and even their personal assets—on the line.

This category covers an incredibly wide range of modern professions:

- Marketing Consultants and Designers: A slick marketing campaign that accidentally infringes on someone else’s trademark could trigger a very expensive legal claim.

- Business Coaches and Mentors: If a client’s business takes a nosedive after following your advice, they could easily turn around and blame you for their losses.

- Web Developers and Software Engineers: A tiny error in a line of code could cause a catastrophic data loss or a major security breach for your client.

For these professionals, thinking about their business structure is a crucial first step. Understanding the pros and cons of operating as a limited company can help clarify their personal liability. At the end of the day, PI insurance provides that vital financial backstop, protecting everything you’ve worked for from a potentially devastating claim.

Decoding Your Policy: What Is and Is Not Covered

A professional indemnity (PI) insurance policy is far more than just a piece of paper; it’s a detailed agreement that spells out exactly when your insurer has your back. Getting to grips with this agreement is critical because a policy is only as good as the protection it actually provides. Let’s break down the fine print in plain English, so you know what’s covered and, just as importantly, what isn’t.

At its heart, professional indemnity insurance is designed to respond when a client claims your professional service caused them a financial loss. This protection generally falls into several key areas.

What Your Policy Typically Covers

While the specifics can vary from one insurer to another, most standard PI policies in the UK are built to cover the financial fallout from mistakes or alleged failures in your professional duties. This is the core purpose of PI insurance.

Common areas of cover include:

- Professional Negligence: This is the big one and the most common reason for a claim. It covers you if you’ve made an error, left something out, or simply failed to meet the standard of care expected in your line of work, causing a client to lose money. Think of an accountant giving flawed tax advice that lands a client with a hefty HMRC penalty.

- Intellectual Property Infringement: This protects you if you unintentionally step on someone else’s copyright, trademark, or confidentiality. A classic example is a graphic designer who accidentally uses a copyrighted image in a client’s branding, leading to legal action.

- Loss of Documents or Data: If you lose or damage client documents or digital data in your care, your policy can cover the costs of replacing or restoring them. This could be anything from misplacing crucial legal papers to a server crash wiping out a client’s project files.

- Defamation (Libel and Slander): Your PI policy can cover the legal costs and any damages if you make a false statement in your professional capacity that harms someone’s reputation.

Actionable Insight: Your policy is there to defend you. Even if a claim is completely baseless, the legal fees to prove your innocence can be astronomical. A good PI policy covers these defence costs from day one, shielding your business from crippling financial strain.

What Your Policy Typically Excludes

Understanding where your cover stops is just as vital as knowing where it starts. Insurers are very clear about what they won’t pay for. These exclusions prevent the policy from covering risks that fall under different types of insurance or are simply uninsurable.

Here are a few common exclusions to look out for:

- Intentional Dishonesty or Fraud: PI insurance covers accidental mistakes, not deliberate wrongdoing. If you knowingly deceive a client or commit fraud, your policy won’t help you.

- Bodily Injury or Property Damage: Claims for physical harm to a person or damage to their property are usually excluded. These risks are what public liability insurance is for—a separate but equally important policy for many businesses.

- Employee-Related Claims: Disputes with your own team, like claims for unfair dismissal or a workplace injury, are not covered by PI. These situations fall under employers’ liability insurance.

- Contractual Liabilities: Your policy won’t cover promises you make in a contract that go beyond your normal professional duty. For instance, you won’t be covered if you promise a client guaranteed results or agree to pay for losses that aren’t a direct result of your negligence.

Real-World Scenarios When a Claim Hits Your Business

It’s one thing to talk about professional indemnity (PI) insurance in theory, but it’s another thing entirely to see how it works in the real world. To really get a feel for its value, let’s walk through a few tangible examples of how a simple client complaint can snowball into a serious financial threat. These stories show just how fast a situation can unravel and why PI insurance is non-negotiable for many businesses.

The risk of facing a claim is much higher than most professionals think. In fact, professional indemnity claims are the most common type of business insurance payout in the UK, accounting for over 26% of all claims. Despite this, a worrying 22% of businesses cancelled their PI cover in 2023 to cut costs, leaving themselves completely exposed. You can explore detailed business insurance statistics from PolicyBee to see more of these trends.

The Consultant and the Costly Advice

Picture this: a seasoned management consultant is hired to whip up a growth strategy for a struggling retail business. After months of hard work, they deliver a comprehensive plan. The big recommendation? A major investment in a new e-commerce platform and a strategic retreat from physical stores. The client trusts the advice and spends a huge sum on the digital overhaul.

Six months down the line, disaster strikes. The client’s revenue has tanked. The fancy new website isn’t performing, and closing the stores has alienated their most loyal customers. Furious, the client files a claim against the consultant, alleging their negligent advice caused over £150,000 in financial losses.

This is exactly where the consultant’s PI insurance jumps into action.

- Immediate Defence: The insurer instantly appoints a specialist legal team to handle the professional negligence claim. Just the fees for these solicitors can quickly climb into the tens of thousands.

- Investigation: The lawyers work with the consultant, digging through every email, report, and piece of data to build a solid defence.

- Settlement: After months of back-and-forth, it’s clear a long court battle would be incredibly expensive for everyone. The insurer’s legal team negotiates a settlement of £75,000 to make the problem go away, which the policy covers in full.

Without PI insurance, the consultant would be staring down the barrel of legal fees and a settlement that could have easily destroyed their business.

The Marketing Agency and the Reputation Wipeout

A buzzy marketing agency lands a contract to launch a new energy drink. Their campaign is bold and edgy, built around a snappy slogan that—unbeknownst to them—is almost identical to one used by an obscure international competitor. The campaign goes live across social media and digital billboards.

Within days, the competitor’s lawyers send a cease-and-desist letter, swiftly followed by a lawsuit for trademark infringement and reputational damage. The client, now facing a PR nightmare and legal threats, points the finger squarely at the marketing agency for not doing their homework. The client sues the agency for the cost of pulling the campaign, rebranding, and settling with the competitor—a whopping £200,000 claim.

Once again, the agency’s PI policy steps up, covering the eye-watering legal defence costs and the eventual settlement paid to the client.

The Business Coach and the Failed Startup

A business coach works closely with the founder of a promising tech startup, offering advice on everything from product development to finding investors. Acting on the coach’s guidance, the founder makes several key hires and enters a partnership that turns out to be a total disaster. The startup fails to secure its next funding round and collapses within a year.

The founder, having lost their personal investment, blames the coach. They allege the guidance was flawed and directly caused the startup’s failure, suing for £50,000 in damages.

Even if a claim seems completely baseless, the cost to defend yourself can be immense. Professional indemnity insurance is your financial shield, ensuring that an allegation doesn’t become a catastrophe by covering the legal costs required to prove your innocence.

In this case, the coach’s PI insurer takes control of the claim. After a deep dive, the appointed solicitors successfully argue that the startup failed due to tough market conditions, not the coach’s advice. The claim is eventually dropped, but the legal fees to get to that point hit over £15,000. The PI policy covered every single penny, protecting the coach’s finances and their professional reputation.

To paint a clearer picture of how these situations play out across different fields, here’s a look at some common claim scenarios.

PI Claim Examples by Profession

| Profession | Example Claim Scenario | Potential Cost Without Insurance |

|---|---|---|

| IT Contractor | A software update they installed contains a bug, causing the client’s entire sales system to go offline for 48 hours, resulting in significant lost revenue. | £50,000 in damages and legal fees. |

| Accountant | Incorrectly files a client’s tax return, leading to a large, unexpected tax bill and penalties from HMRC. The client sues for the penalty amount and professional fees. | £25,000 to cover penalties and legal costs. |

| Architect | A design flaw in their building plans is discovered mid-construction, requiring expensive structural changes and causing project delays. | £120,000 for rectification work and client compensation. |

| Graphic Designer | Accidentally uses a copyrighted image in a client’s national advertising campaign, resulting in a copyright infringement lawsuit. | £30,000 in settlement and legal defence costs. |

| Recruitment Consultant | Fails to perform adequate background checks on a candidate who is later found to have falsified their qualifications, causing damage to the client’s business. | £40,000 to cover the client’s losses and legal expenses. |

As you can see, a simple mistake can have devastating financial consequences, regardless of your profession. These examples underscore why having the right protection in place isn’t just a good idea—it’s essential for survival.

How Your Insurance Premium Is Really Calculated

Ever wondered what goes on behind the scenes when an insurer works out your professional indemnity quote? It’s not just a number pulled out of thin air. Instead, it’s the result of a detailed risk assessment where underwriters weigh up several key factors to figure out the likelihood of a claim being made against you.

Understanding these factors is crucial because it gives you a degree of control. If you actively manage your business risks, you can present yourself as a much more attractive prospect to insurers and potentially bring that premium down. Let’s pull back the curtain on how this pricing process really works.

Your Profession and Its Inherent Risks

The first thing any underwriter looks at is your line of work. It’s a simple fact that some professions are seen as higher risk than others, purely because of the nature of the advice or services they provide. For example, an architect whose design flaw could lead to multi-million-pound rectification works faces a completely different level of risk than a freelance copywriter.

Insurers pore over historical claims data for your specific industry to predict future trends. Professions that handle sensitive data, large sums of money, or make decisions with huge financial consequences for clients—think accountants, solicitors, and IT security consultants—will almost always have higher base premiums.

Business Size and Turnover

Your annual turnover is a key metric for insurers. It acts as a rough-and-ready guide to the scale of your operations and the size of the contracts you’re handling. A business with a £1 million turnover is likely working on bigger, more complex projects than a sole trader earning £50,000 a year.

A higher turnover suggests that if a mistake happens, the resulting claim could be for a much larger amount. This doesn’t mean you’re penalised for growing your business, but your premium will naturally scale alongside your revenue to reflect the increased risk exposure. Getting a grip on your income is vital, and our guide on managing cash flow for your small business can offer some really helpful strategies.

Your Claims History

Nothing speaks louder to an insurer than your track record. A clean claims history—meaning no claims have been made against you in the past—is the best possible indicator of good risk management. It tells an underwriter that you have solid processes in place and are less likely to run into trouble down the line.

On the flip side, if you’ve had claims before, your premium will almost certainly be higher. Insurers will want to know exactly what happened, what steps you’ve taken to prevent it from happening again, and whether there’s a pattern of recurring issues.

Actionable Insight: Proactive risk management is your most powerful tool for influencing your premium. Robust client contracts, clear service level agreements, and documented quality control checks are not just good business practice—they are tangible proof to an insurer that you take your professional responsibilities seriously.

The Wider Insurance Market

Finally, some factors that affect your premium are completely out of your hands. The insurance market moves in cycles. During a ‘hard market’, insurers get more cautious, there’s less capacity to take on risk, and premiums rise across the board. In a ‘soft market’, competition heats up between insurers, leading to more competitive pricing for you.

The UK PI market has seen a dramatic shift recently. After a tough ‘hard market’ from 2019-2022 where rates soared, prices started to fall in 2024. Experts predict this trend will continue, with potential rate drops of 15-20% into late 2025, especially for well-managed firms with strong risk controls. It just goes to show how demonstrating good practice can really pay off when market conditions improve.

Your Action Plan for Securing the Right Cover

Getting your head around professional indemnity (PI) insurance can feel like a chore, but it doesn’t have to be. With the right approach, you can move from understanding the basics to getting the perfect cover in place for your business. This is your straightforward, step-by-step guide to making a confident choice and ensuring your business is properly protected from potential claims.

Let’s get started. The first port of call, long before you start looking at quotes, is to get a really clear picture of your own unique risks.

Step 1: Assess Your Risks and Required Cover Level

First things first, take an honest look at your business operations. What services do you actually provide, and what could go wrong? Think about the worst-case scenarios if a mistake was made. You need to consider the size of your clients and the potential financial fallout for them if an error on your part caused them a significant loss.

Next up, dig out your client contracts. Many will state the minimum level of PI cover you need to have, which often sits somewhere between £1 million and £5 million. If you’re a member of a professional body, they’ll likely have their own mandatory requirements too. Use these figures as your starting point, but always ask yourself if your specific risks mean you should aim for a higher limit.

Step 2: Prepare Your Business Information

To get an accurate quote, insurers need to understand your business inside and out. Being organised not only makes the process quicker but also paints you as a well-managed, lower-risk business, which can only help.

Get the following details and documents ready:

- Business Details: Your company’s registered name, address, and Companies House number.

- Financials: Your annual turnover from the last financial year and a realistic projection for the next one.

- Services: A clear, detailed description of the professional services you provide.

- Contracts: Have a few examples of your client contracts or your standard terms of business to hand.

- Claims History: A record of any previous claims made against you, even if nothing came of them.

Step 3: Compare Quotes Beyond the Price Tag

When the quotes start rolling in, it’s all too easy to just grab the cheapest one and be done with it. But the best value is rarely the lowest price. You need to look closely at the policy details to make sure you’re comparing apples with apples.

Actionable Insight: A cheap policy with major exclusions or a sky-high excess could leave you dangerously exposed right when you need it most. It’s all about finding the right balance between the cost and the quality of the cover on offer.

Pay special attention to the policy excess – that’s the amount you have to cough up towards any claim. Also, check the retroactive date, as this determines how far back the policy will cover work you’ve done in the past.

Showing insurers you’re on top of your game can also make a difference. Putting solid internal processes in place, like comprehensive regulatory compliance training, demonstrates good risk management. For new companies and sole traders, simply establishing a formal UK business presence with a proper registered office address is another crucial step. It builds credibility and can help you secure better insurance terms right from the start.

Frequently Asked Questions

When you’re sorting out professional indemnity insurance, a few common questions always seem to pop up. Getting straight answers is the key to picking the right cover without any guesswork. Here are the queries we hear most often from UK business owners and sole traders.

What’s the Difference Between Professional Indemnity and Public Liability Insurance?

This is easily the most common point of confusion, but the distinction is actually quite simple. While they’re both essential types of business insurance, they protect you from completely different kinds of trouble.

Think of it this way:

- Professional Indemnity (PI) Insurance is all about the quality of your professional services or advice. It steps in when a client claims they’ve suffered a financial loss because of a mistake you made in your work, like negligence or a costly error.

- Public Liability (PL) Insurance deals with the physical world. It covers claims for injury or property damage that your business activities cause to someone else. If a client trips over your laptop cable during a meeting and breaks their wrist, that’s a public liability issue.

In short, PI is for financial fallout from your advice, while PL is for physical damage from your actions.

How Much PI Cover Does My Small Business Need?

There’s no magic number here; the right amount of cover is entirely down to your specific business. However, you can figure out a sensible figure by looking at a few key things:

- Your Contracts: Always check your client contracts first. Many will flat-out tell you the minimum level of PI cover you need to have, which is often between £1 million and £2 million.

- Regulatory Rules: Are you a member of a professional body like the ICAEW for accountants or the SRA for solicitors? If so, they’ll have their own mandatory minimum cover levels you must meet to remain compliant.

- The Worst-Case Scenario: Be honest with yourself. What’s the maximum financial damage a mistake could cause for your biggest client? Your cover needs to be high enough to handle that nightmare scenario without bankrupting you.

What Is a Retroactive Date and Why Does It Matter So Much?

The retroactive date is a hugely important detail on your policy. It’s the date from which your past work is officially covered. If a claim comes in relating to a project you finished before this date, your insurer won’t cover it. Simple as that.

Actionable Insight: To make sure you’re fully protected, it’s vital that your retroactive date is set to the day you first started trading or the date your very first PI policy began. Any gap in cover leaves your entire work history dangerously exposed.

What Is a Policy Excess?

The excess is simply the amount you agree to pay out of your own pocket towards a claim before your insurance kicks in to cover the rest.

For example, if you face a claim for £20,000 and your policy has a £500 excess, you’d pay the first £500, and your insurer would handle the remaining £19,500. Insurers use an excess to discourage lots of small, trivial claims and to ensure you share a tiny piece of the risk.

When you’re arranging business insurance, establishing a credible UK presence is a crucial first step. Acorn Business Solutions can provide you with a professional registered office address, helping you meet compliance requirements and present your business in the best possible light. Learn more and set up your business for success at https://acornbusinesssolutions.com.

Related Topics

What is a company secretary

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

How Do You Redirect Your Mail in the UK?

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

Top accounting courses for small business in the UK (2025)

Discover accounting courses for small business in the UK. Compare top options, pricing, and formats

UK Business Bank Accounts With No credit Checks

Discover UK business bank accounts with no credit checks. This guide explains your options and eligibility

Managing cash flow for small business: Quick tips

Discover managing cash flow for small business with practical steps to forecast, optimize liquidity,

Your Guide to the company unique tax reference number

Discover what the company unique tax reference number is, why you need it, and how to locate yours quickly.