A Guide to Business Loan Requirements

When it comes to securing a business loan, lenders are all asking the same fundamental question: is your business a safe bet? They need solid proof that you’re a reliable investment. The main business loan requirements are all about showing them your company’s financial stability, its potential for growth, and that you know how to manage debt responsibly. It’s your job to build a compelling case backed by hard numbers and a crystal-clear vision for the future.

What Lenders in the UK Really Look For

Trying to get a business loan in the UK can sometimes feel like aiming at a moving target. The wider economic climate has a huge effect on how confident lenders feel, and that directly shapes how they view your application. Getting inside their heads is the first step to putting together a proposal that actually works.

Lenders aren’t just scanning your balance sheet; they’re trying to understand the whole story of your business. They want to see a clear narrative that proves you’re stable and highlights your potential. It’s about much more than just profit—it’s about showing resilience and having a proper plan for what comes next.

The Current Lending Landscape

The latest data paints a picture of cautious optimism among UK lenders. In the first quarter of 2025, gross lending to SMEs hit nearly £4.6 billion, which is a healthy 14% jump from the previous year. While that’s a good sign that their appetite for investment is returning, the total amount is still lagging behind pre-pandemic figures. In short, lenders are open for business, but they’re still being selective. You can dig deeper into the current SME finance trends in UK Finance’s latest report on their official website.

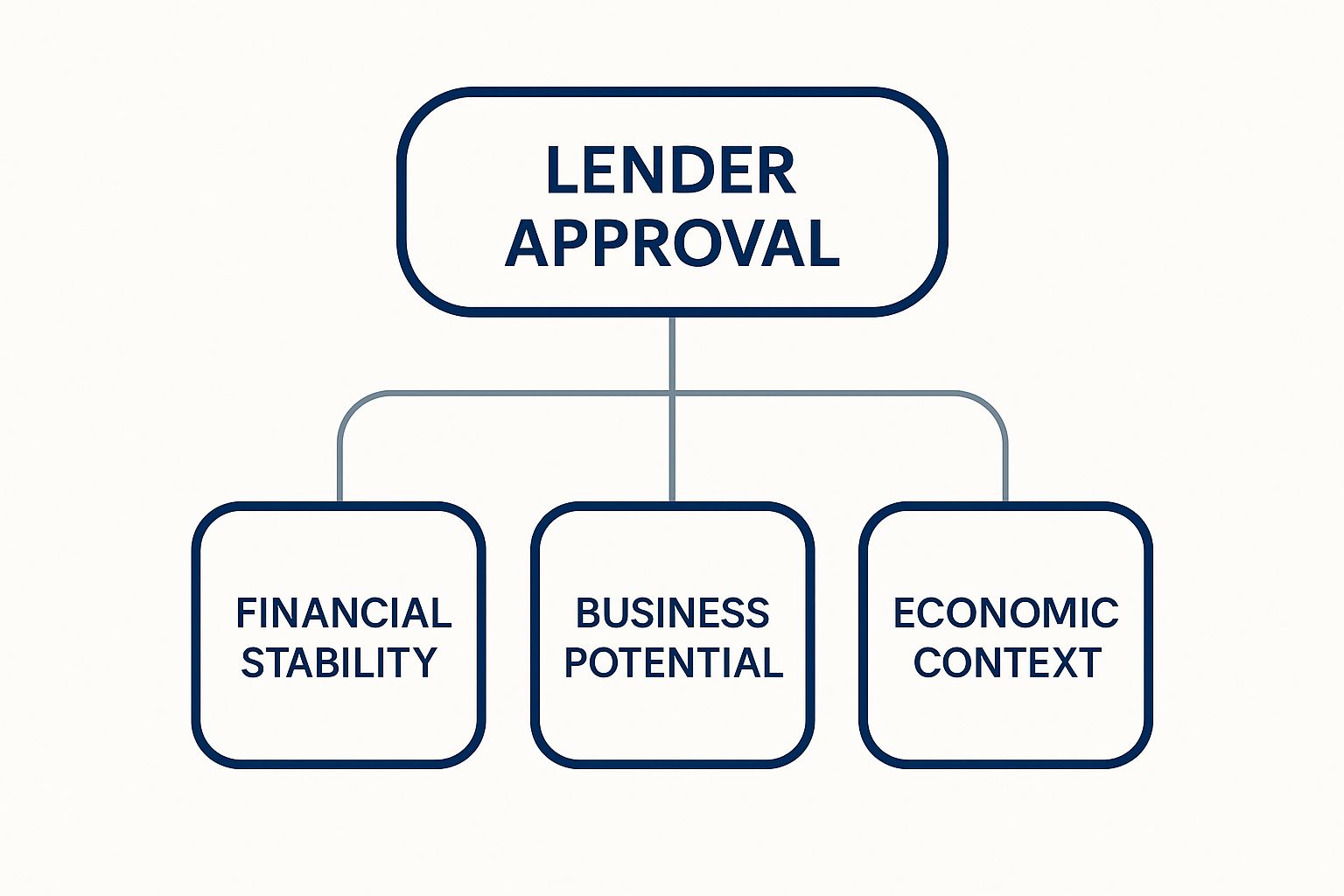

This infographic breaks down the core pillars of what gets a loan application over the line.

As you can see, a winning application is a balancing act. It needs to show robust financial health, a convincing vision for growth, and an awareness of the current economic climate.

Building a Persuasive Case

To meet these expectations, your application needs to be a masterclass in telling a story with data. It’s not enough to just hand over your financial statements and hope for the best. You have to connect the dots for the lender.

A strong loan application doesn’t just present facts; it builds confidence. It shows a lender that you not only understand your business’s current position but also have a credible and strategic plan to navigate the future.

For example, instead of just showing a year-on-year revenue increase from £80,000 to £110,000, explain why it happened. You might say, “Our 37.5% revenue growth was driven by a targeted social media campaign in Q3 that expanded our customer base by 25% and a new product line that accounted for £15,000 in sales.” This context turns your numbers from static figures into powerful evidence of a well-run, forward-thinking business. Your goal is to leave them with no doubt that you’re a responsible and capable borrower.

The Six Pillars of a Strong Loan Application

When you’re trying to figure out what lenders are really looking for, it helps to break down their requirements into six core pillars. Think of these as the legs of a table—if one is wobbly, the entire structure is unstable. Getting these areas right isn’t just about ticking boxes; it’s about building a compelling case that shows lenders you’re a safe bet.

Each pillar is designed to answer a fundamental question a lender has about your business and your ability to repay their money. Once you understand the ‘why’ behind each request, you can present your business in the strongest possible light.

The Core Components of Your Application

Here’s a practical look at the six pillars that underpin almost every business loan assessment in the UK.

- Your Credit History: This is all about your track record. Lenders want to see how you’ve handled borrowing in the past, both for you personally and for your business. It’s the most direct predictor they have for how you’ll manage this new loan. For example, a consistent history of paying off a business credit card in full each month is a strong positive signal.

- Your Financial Health: This pillar is a snapshot of your business right now. Lenders will pour over your revenue, profits, and cash flow to make sure your business is financially stable enough to take on new debt repayments without buckling. A practical example would be showing at least three to six months of bank statements that reveal a healthy, positive cash balance.

- Your Business Viability: This is your chance to tell your forward-looking story. Your business plan needs to convince the lender you have a clear, realistic strategy for growth and a genuine place in the market. It shows them their money is being invested in a solid plan, not just a vague hope.

- Available Collateral: Think of this as the lender’s safety net, primarily for secured loans. If you have assets like property, machinery, or even high-value invoices, you can offer them as security. For instance, a construction company could use a £50,000 excavator as collateral for a £30,000 loan.

- Your Trading History: This pillar is all about demonstrating stability and experience. Lenders feel much more comfortable with businesses that have been up and running for a while, typically at least one to two years. A proven track record is hard to argue with.

- Your Revenue Consistency: Predictability is key here. Wildly fluctuating income can be a massive red flag for lenders. For example, a subscription-based software company with predictable monthly recurring revenue (MRR) is often seen as less risky than a project-based business with lumpy, inconsistent income.

To help you keep track, the table below summarises what each pillar is, why it matters, and the key piece of evidence you’ll need.

The Six Pillars of a Loan Application at a Glance

This table breaks down the core components lenders evaluate to determine if your business is a good candidate for funding.

| Pillar | Why Lenders Care | Key Document or Metric |

|---|---|---|

| Credit History | It predicts your future repayment behaviour. | Credit Score (Personal & Business) |

| Financial Health | It confirms you can actually afford the loan. | Profit & Loss Statement, Bank Statements |

| Business Viability | It shows the loan is a smart, calculated investment. | A Detailed Business Plan |

| Available Collateral | It reduces the lender’s financial risk. | Asset Valuation Reports |

| Trading History | It proves your business isn’t a fleeting idea. | Years in Operation |

| Revenue Consistency | It demonstrates reliable, predictable cash flow. | Monthly Revenue Statements |

Focusing on strengthening these six areas is the single most effective way to prepare for a successful business loan application. It puts you in control of the narrative and allows you to present your business with confidence.

Proving Your Financial Health

Your financial documents are far more than just a record of transactions; they tell the story of your business’s journey and offer a glimpse into its future. Lenders pore over these documents to judge your stability and reliability, making them the absolute cornerstone of your application.

Think of it this way: you’re asking someone to invest in your vision. Your financials are the evidence that proves your vision is grounded in reality. The two most critical pieces of that evidence are your credit score and your financial statements.

Credit Scores: Personal and Business

One of the very first things a lender will check is your credit history. They’ll usually want to see both your personal credit score and, if you have one, your business credit score.

Your personal credit score is essentially your individual financial reputation. For sole traders and brand-new businesses, this score is especially vital because lenders will see you and your business as one and the same. A solid history of paying your personal bills on time really works in your favour here.

Your business credit score, on the other hand, reflects your company’s track record of managing its own debts, like paying suppliers or handling previous loans. A strong business score shows you manage company finances responsibly, but be warned – a weak personal score can still raise a red flag for the lender.

Your Financial Statements, Explained

Financial statements are the official report cards of your business’s performance. There are three key documents that work together to provide a complete picture: the profit and loss statement, the balance sheet, and the cash flow statement.

To make this crystal clear, let’s imagine a local coffee shop called “The Daily Grind,” which is applying for a loan to buy a shiny new espresso machine.

- Profit and Loss (P&L) Statement: This shows their income versus their expenses over a specific period, like a quarter or a year. The lender would see all the revenue from coffee sales minus the cost of beans, milk, staff wages, and rent. A consistent profit demonstrates the business is sustainable.

- Balance Sheet: This is a snapshot of the business’s financial health at a single moment in time. It lists assets (what The Daily Grind owns, like its current equipment and the cash in its bank account) and liabilities (what it owes, like unpaid supplier invoices). A healthy balance sheet shows that assets comfortably outweigh liabilities.

- Cash Flow Statement: This might just be the most crucial document of all. It tracks the actual cash moving in and out of the business – the real money in the bank. Lenders look for positive cash flow, as it proves the coffee shop has enough ready money to cover its day-to-day operations and the new loan repayments. You can get a head start on this by using a tool like this free cash flow forecast template to map out your projections.

Lenders are deeply wary of inconsistent cash flow. Even a profitable business on paper can fail if it runs out of cash to pay its bills, making this statement a critical test of your operational stability.

Interestingly, despite how important these documents are, many UK businesses seem reluctant to apply for funding. Data from mid-2024 shows that only 1.5% of UK SMEs applied for a bank loan, a figure far lower than the nearly 20% seen in the Euro area.

This suggests that really getting to grips with these business loan requirements is a key step in building the confidence to go out and seek the finance your business deserves. You can find out more about the trends in small business access to finance on the official government website.

Crafting Your Business Plan to Win Funding

If your financial statements are a snapshot of your business’s past, your business plan is the map showing a lender exactly where you’re headed next. It’s far more than a document; it’s your strategic pitch, the story you tell to convince someone that your business is a smart, calculated investment.

A generic, fill-in-the-blanks template just won’t do the job. Lenders see hundreds of these, and they can spot a lazy effort a mile off. Yours needs to be sharp, packed with real data, and focused on proving you have a firm grip on your market and a realistic plan to grow.

The Story Your Plan Must Tell

Think of your business plan as a persuasive argument, with every section providing the evidence. It has one core job: to draw a clear, undeniable line from the loan you’re asking for to your future success.

Lenders zoom in on three parts above all others:

- Executive Summary: This is your first impression and, frankly, the most critical part. It’s a powerful, punchy overview of your entire plan that has to grab their attention from the first sentence.

- Market Analysis: This is where you prove you’ve done your homework. You need to show you know your target customer inside out, what your competitors are up to, and where you fit into the bigger industry picture.

- Financial Projections: Here’s where your strategy gets turned into hard numbers. Lenders need to see sensible, well-reasoned forecasts for your revenue, profits, and cash flow for the next three to five years, showing precisely how their money fuels that growth.

From Passion to Projections

A lender wants to feel your passion, but they make their decisions based on cold, hard data. Your business plan is the bridge that connects the two.

For instance, don’t just say you have a “loyal customer base.” Prove it with data. A practical example would be: “Our customer retention rate is 85% year-on-year, and our average customer lifetime value is £1,200, which is 20% above the industry average.”

The same goes for your financial projections. These can’t be numbers plucked from thin air. They must be grounded in your past performance, solid market research, and a clear list of assumptions. If you’re asking for £25,000 to buy a new 3D printer for your manufacturing business, your forecasts must show the direct impact. For example: “The new printer will increase production capacity by 40%, allowing us to take on two new client contracts worth an estimated £4,000 per month in additional revenue.”

A business plan is your roadmap. It tells a lender not just where you want to go, but the exact route you’ve planned to get there, including how you’ll handle any detours along the way.

The executive summary is your chance to make a powerful first impression. To really nail it, it’s a great idea to review some well-written business plan executive summary examples to see how to frame your pitch for maximum impact. A strong plan doesn’t just show your vision; it proves you’re a strategic thinker, turning a simple loan application into a compelling investment proposal.

Understanding Collateral and Personal Guarantees

Let’s demystify two terms that often cause a bit of anxiety for business owners when they see them on a loan application: collateral and personal guarantees. Both are all about reducing the lender’s risk, and getting your head around them is vital for choosing the right kind of funding for your business.

Think of collateral as a security deposit for your loan. It’s a specific, valuable asset you pledge to the lender, which they have a right to claim if you can’t repay the debt. This whole arrangement is the foundation of what’s known as a secured loan.

Offering this kind of security makes lenders feel much more comfortable. In return, you’ll often find they offer better interest rates or are willing to lend larger amounts. It gives them a tangible fallback plan if your business runs into serious trouble.

What Qualifies as Collateral?

Lenders are interested in assets they can realistically value and, if the worst happens, sell to get their money back. So, not everything you own will make the cut.

Common examples of business assets used as collateral include:

- Commercial Property: A bakery owner might use the shop premises they own to secure a loan for a major refurbishment.

- Equipment and Machinery: A haulage company could use one of its £80,000 lorries as collateral for a £40,000 loan to cover operational costs.

- Inventory: A fashion retailer could use its current season’s stock, valued at £50,000, to secure a short-term loan for a new marketing campaign.

- Accounts Receivable: A marketing agency with £20,000 in unpaid invoices from reliable blue-chip clients could use these invoices as security for a loan.

Before they agree, a lender will almost always require a formal valuation to determine the asset’s true worth. They’ll then typically offer a loan for a percentage of that value, known as the Loan-to-Value (LTV) ratio.

Personal Guarantees: The Ultimate Promise

While collateral is tied to business assets, a personal guarantee is linked directly to you, the owner. By signing one, you are making a legally binding promise to repay the business debt using your personal assets if the company is unable to.

That means things like your home, personal savings, or car could be on the line. It’s a massive commitment that blurs the line between your business and personal finances, and it’s often a requirement for unsecured loans where no specific collateral is pledged.

A personal guarantee is a lender’s ultimate safety net. It shows them how personally committed you are to the business’s success, because you’re willing to put your own financial wellbeing on the line.

Because the stakes are so high, it’s vital to have solid legal protections in place before you even think about signing. It’s well worth taking the time to learn how to protect your business with contracts and agreements to ensure you fully grasp the implications. Making an informed decision here is absolutely critical for your personal financial security.

Choosing the Right Lender for Your Business

Finding the right lender isn’t about hunting for a single “best” option. It’s more like matchmaking – you need to find a lender whose criteria and appetite for risk align with your business’s unique story and numbers.

The UK market is full of choices, from big high street names to nimble online players. Targeting your application properly from the very beginning saves a massive amount of time and frustration, and it dramatically boosts your chances of getting a “yes.” A startup with only six months of trading, for example, will likely get an instant rejection from a traditional bank but could be the perfect fit for a modern, tech-driven lender.

High Street Banks vs Challenger and Online Lenders

The world of business lending has changed a lot. While the big high street banks are still a major source of funding, their lending criteria can be incredibly tough. They typically favour well-established businesses with years of trading history, spotless credit, and solid assets.

This is where challenger banks and alternative online lenders have stepped in, becoming a lifeline for small and medium-sized businesses (SMEs). They often use smart technology to make faster decisions, and they tend to focus more on your recent cash flow and revenue rather than demanding a long, perfect track record. This flexibility has made them the go-to choice for newer businesses and those who don’t fit the traditional mould.

It’s clear that challenger and specialist lenders are now a dominant force. They were responsible for a staggering 62% of all government-backed lending in 2024, signalling a major shift towards more adaptable funding for UK businesses.

By the end of 2024, the total outstanding loan stock for UK SMEs had reached a massive £179 billion, with new applications continuing to rise. This shows just how much demand there is for finance and highlights the critical role these newer lenders are playing in the economy. You can dig into more of this data on SME lending trends over at the British Business Bank.

To help you figure out where you fit in, the table below gives a simple comparison of the main types of lenders.

Comparing Different Types of UK Business Lenders

Understand the key differences in requirements and features to find the lender that best matches your business needs.

| Lender Type | Typical Credit Score | Loan Amounts | Application Speed |

|---|---|---|---|

| High Street Banks | Excellent (700+) | £25k – £1M+ | Slow (Weeks) |

| Challenger Banks | Good to Excellent | £10k – £500k | Moderate (Days) |

| Online Lenders | Fair to Good (600+) | £1k – £250k | Fast (24-48 Hours) |

This quick comparison should give you a better feel for which door to knock on first. If you have a long, profitable history and aren’t in a rush, a high street bank might offer the best rates. But if speed is essential and your business is newer, an online lender is almost certainly a better bet.

Got Questions About Business Loans? We Have Answers

Even with all the preparation in the world, it’s natural to have a few lingering questions when you’re about to apply for a business loan. Stepping into the world of finance can feel a bit daunting, so let’s clear up some of the most common queries business owners have.

Think of this as a final run-through before you submit your application. We’ll tackle the practical concerns head-on, so you can move forward with total confidence.

Can I Get a Business Loan with Poor Personal Credit?

It’s tougher, but definitely not a deal-breaker. While high street banks can be very rigid about credit scores, many alternative and specialist lenders in the UK look beyond your personal history. They’re often more interested in the health of your business right now—specifically, your recent revenue and cash flow.

Be prepared, though; you’ll likely face higher interest rates as the lender is taking on more perceived risk. You can strengthen your case by presenting a rock-solid business plan with conservative financial forecasts. If you have assets you can offer as security, that collateral can also make a huge difference in getting a “yes.”

How Much Revenue Does My Business Need to Show?

There’s no single magic number here. The minimum turnover lenders look for varies wildly depending on the type of loan and the lender themselves. For many UK online lenders, a common starting point is an annual turnover somewhere between £50,000 and £100,000.

Traditional banks might not give you a specific figure, but they’ll be scrutinising your revenue against your outgoings. What they really want to see is a consistent cash flow that proves you can comfortably handle the loan repayments on top of all your existing business costs.

A lender’s focus isn’t just on your top-line revenue. They care most about your net operating income—the profit left after all your day-to-day expenses are covered. That’s the figure that truly shows if you can afford to take on new debt.

What Are the Most Common Reasons for Rejection?

Knowing where others have stumbled is the best way to avoid falling into the same traps. The most frequent reasons a loan application gets turned down include:

- A shaky credit history: This covers both your personal and business credit reports.

- Not enough cash flow: Lenders need to be certain you have enough money coming in each month to make repayments without struggling.

- A weak business plan: A plan that feels unrealistic, rushed, or poorly researched is a major red flag for any lender.

- A short trading history: Many lenders get nervous about businesses that have been operating for less than one or two years.

- No collateral to offer: This is often a hurdle for businesses trying to secure larger loans, which typically need to be backed by an asset.

Another surprisingly common mistake is simply applying for the wrong type of finance for your business’s needs or stage of growth. Taking the time to prepare your documents properly and choosing the right lender from the outset will help you sidestep these common pitfalls and make your application much stronger.

Related Topics

Professional Indemnity Insurance

Discover what is professional indemnity insurance, why your business needs it, and how it shields you from costly client claims.

What is a company secretary

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

How Do You Redirect Your Mail in the UK?

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

Top accounting courses for small business in the UK (2025)

Discover accounting courses for small business in the UK. Compare top options, pricing, and formats

UK Business Bank Accounts With No credit Checks

Discover UK business bank accounts with no credit checks. This guide explains your options and eligibility

Managing cash flow for small business: Quick tips

Discover managing cash flow for small business with practical steps to forecast, optimize liquidity,