How to Close a Dormant Company

How to Close a Dormant Company – So, you have a dormant company sitting there and you’re wondering what to do with it. Closing it down is usually a pretty straightforward affair in the UK, typically done through what’s called a voluntary strike-off using form DS01. This is the go-to route if your company has never traded, or has ceased trading, and has no assets or debts. It’s a clean, low-cost way to formally shut down a business that’s run its course.

Knowing When to Close Your Dormant Company

Before you start filling out any forms, it’s worth taking a final moment to be absolutely sure that closing the company is the right move. This isn’t about second-guessing yourself, but more of a final gut-check to ensure you’re acting deliberately, not just reacting to the minor admin burden of keeping it on the books.

Common Reasons for Dissolution

Directors decide to dissolve dormant companies for all sorts of practical reasons. It’s rarely about failure; more often than not, it’s about tidying up loose ends and just simplifying things.

Here are some practical examples of why a director might close a dormant company:

- The side project that never got off the ground: You registered “Artisan Coffee Roasters Ltd” with a friend, but life got in the way and you never bought the first bag of beans. The company exists only on paper.

- A Special Purpose Vehicle (SPV) that’s done its job: An SPV named “123 High Street Holdings Ltd” was set up to hold the freehold for a property development. The project is now complete, the property sold, and the SPV is no longer needed.

- The business idea you registered but never pursued: You smartly secured the name “Eco Delivery Solutions Ltd” but then accepted a full-time job offer. The company has served its purpose of reserving the name, but now it’s just an administrative task.

- A desire for less admin: You simply want to shed the legal responsibilities of filing a confirmation statement and dormant accounts each year, reducing your mental clutter.

Weighing the Costs Against the Benefits

Keeping a dormant company open isn’t exactly expensive, but it’s not free of obligations either. You’re still on the hook for filing a confirmation statement and dormant company accounts every year. While the financial cost is minimal—usually just the Companies House filing fee—the real cost can be the nagging responsibility and the risk of penalties if you forget and miss a deadline.

Deciding whether to close a dormant company often boils down to one simple question: Does the potential future value of this company outweigh the mental and administrative cost of keeping it alive today? For most people, the clarity of a clean slate is worth far more than a ‘what if’.

This thinking is becoming more and more common. By the end of June one year, there were 458,295 companies in the process of dissolution, a 14.27% increase from the previous year. This jump shows a clear trend among business owners to efficiently close down entities that are no longer serving a purpose. You can dig into the official numbers in the government’s report on corporate statistics and dissolution trends.

Choosing Your Closure Path: Strike-Off or Liquidation?

Right, so you’ve decided it’s time to close your dormant company. The next big question is how you go about it. This isn’t a one-size-fits-all situation, and picking the wrong route can lead to a world of legal headaches and wasted money. In the UK, you’ve got two main options on the table: a voluntary strike-off or a formal liquidation.

For the overwhelming majority of dormant companies, the decision is refreshingly simple. A voluntary strike-off, often just called dissolution, is the most common, cheapest, and most straightforward way to close up shop. It’s designed specifically for companies that are solvent – meaning they can comfortably pay all their debts – but just aren’t needed anymore.

The Simplicity of a Voluntary Strike-Off

Think of a strike-off as a simple housekeeping task. You’re just asking Companies House to neatly remove your company’s name from their official register. It’s the perfect choice if your dormant company has a clean slate: no outstanding debts, no lingering assets, and it hasn’t traded for at least three months.

Here’s a classic scenario. You registered ‘Innovate Web Ltd’ a few years back for a freelance gig. That project is long finished, the company has zero debts, the bank account is empty, and it’s just been sitting there, dormant. In this case, applying for a strike-off is a no-brainer. It provides a clean break with minimal fuss and a small filing fee.

Actionable Insight: If your company’s balance sheet is zero (no assets, no liabilities) and it has no active business operations, the strike-off route is almost certainly for you. It was designed for exactly this kind of uncomplicated, uncontroversial closure.

When Formal Liquidation Becomes Necessary

Liquidation, on the other hand, is a whole different beast. It’s a much more formal, legally intensive process and not something you’d ever choose for a simple dormant company unless there are some financial skeletons in the closet. This path becomes mandatory if the company is insolvent, which means its debts are greater than its assets and it simply can’t pay what it owes.

Even a dormant company can have liabilities. Imagine ‘Property Holdings SPV Ltd’ was set up to hold a property. It might have an outstanding director’s loan or a small, forgotten bill from an old accountant. If there’s no money or assets in the company to clear those debts, you cannot legally apply for a strike-off. Trying to do so could be viewed as an attempt to dodge your creditors, which can have serious personal consequences for the directors.

Economic pressures often bring these issues to the surface. For instance, in one recent August, there were 2,048 company insolvencies in England and Wales, a 6% increase from the previous year. This figure shows just how many businesses are facing financial strain, and it’s a stark reminder of why it’s vital for dormant companies to be absolutely sure they are debt-free before opting for the simple strike-off path. You can dig into the latest numbers by reviewing the UK company insolvency statistics.

Ultimately, you have to be brutally honest about your company’s financial position. A strike-off is a formal declaration that your company is solvent and has no one left to pay.

Strike-Off vs. Liquidation: Which Path to Choose?

Making the right choice here is crucial. One path is a straightforward administrative task you can handle yourself, while the other involves licensed professionals and a formal legal procedure. To help you decide, this table breaks down the key differences.

| Consideration | Voluntary Strike-Off (Dissolution) | Liquidation (e.g., MVL/CVL) |

|---|---|---|

| Ideal For | Solvent, dormant companies with no assets or liabilities. A clean and simple closure. | Insolvent companies that cannot pay their debts, or solvent companies with significant assets to distribute. |

| Cost | Very low – typically just the Companies House filing fee. | Significantly higher, involving fees for a licensed Insolvency Practitioner. |

| Complexity | Simple administrative process managed by the directors. | Formal legal process overseen by a court-appointed liquidator. |

| Timeline | Relatively quick, usually taking around three to four months if there are no objections. | Can be a lengthy process, often taking many months or even years to complete. |

| Key Requirement | The company must be solvent and have ceased trading for at least three months. | Triggered by insolvency or a formal decision to wind up a company with assets. |

After looking at this, the correct path for your dormant company should be much clearer. If you’re in the strike-off camp, you’re looking at a relatively quick and painless process. If liquidation seems more appropriate, it’s time to seek professional advice.

Your Pre-Closure Checklist for a Smooth Process

Applying to strike off your company isn’t the first thing you do—it’s one of the last. Before you can even think about filling in that DS01 form, you need to get the company’s affairs completely in order. Rushing this stage is the single most common reason applications get rejected, turning what should be a simple process into a frustrating mess.

Think of it like preparing a house for sale. You wouldn’t put it on the market with unpaid bills and clutter everywhere. It’s the same principle here; you must tidy up your company’s administrative and financial loose ends for a clean, final exit. This means getting everything squared away with both Companies House and HMRC.

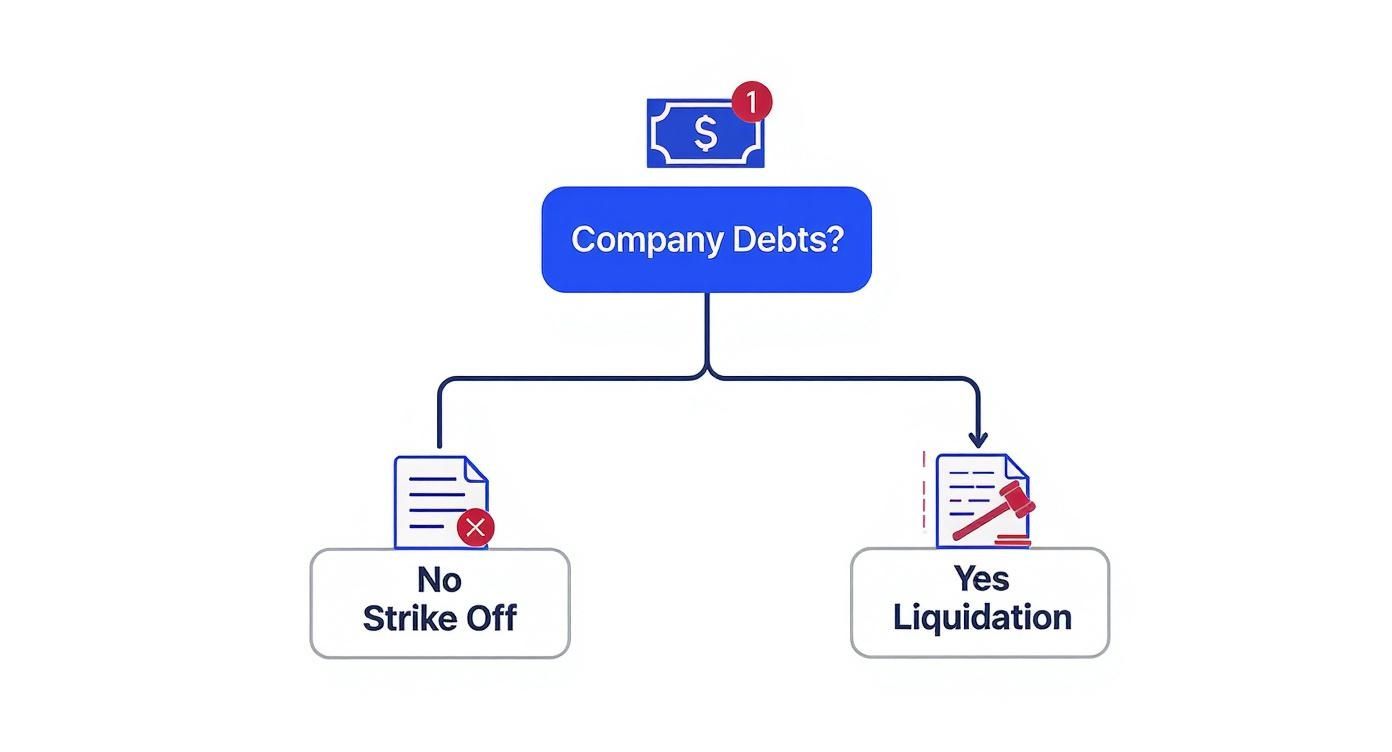

This decision tree gives a quick visual guide on the fundamental choice you face, which all comes down to the company’s financial state.

As you can see, the presence of any company debt immediately pushes you down the more formal liquidation route. That’s why clearing every last liability is a non-negotiable first step if you want a simple strike-off.

Finalise Your Companies House Filings

Before you can ask Companies House to remove your company from the register, you have to be fully up to date with your statutory filings. They simply won’t close a company that has outstanding compliance duties. It’s an easy check for them to perform, and any oversight will get your application bounced straight back to you.

Your two main priorities here are:

- Final Dormant Company Accounts: You must file dormant accounts for any financial year that has passed. For example, if your year-end is 31st December and you decide to close the company in February, you must first file the dormant accounts for the period that just ended in December.

- Confirmation Statement: Make sure your confirmation statement is current. If it’s overdue, it has to be filed before you proceed. This just confirms that the company’s details on the public record are correct at the point you apply for closure.

Failing to do this is such a common mistake. A director might assume that because the company is closing, these last filings don’t matter. But in reality, they are an absolute prerequisite for a successful application. For anyone who finds these final admin tasks a bit of a headache, looking into professional dormant company management can really simplify things.

Settle All Financial and Tax Matters

Once your Companies House record is tidy, your next focus is to make the company financially sterile. This means dealing with HMRC, shutting down bank accounts, and sorting out any internal loans. Every penny needs to be accounted for and every official registration closed down.

Start by getting in touch with HMRC to tie up any loose ends. If the company was ever registered for Corporation Tax, you must tell them it has ceased trading (or indeed, never traded) and that you intend to have it struck off. They’ll then update their records and issue any final notifications.

You should also take care of any other tax registrations:

- VAT De-registration: If the company was ever VAT registered, you have to formally de-register. You cannot strike off a company with an active VAT registration.

- PAYE Scheme Closure: In the same way, if you ever had a PAYE scheme for employees (even if it was just for the directors), this must be officially closed.

Actionable Insight: The golden rule before applying for a strike-off is to achieve a zero balance sheet. This means no assets, no liabilities, no money in the bank, and no debts owed to anyone—including the taxman or the directors themselves.

Close the Company Bank Account

This step is critical and, if overlooked, can have serious consequences. Before the company is dissolved, you absolutely must close its bank account and transfer any remaining funds out.

Here’s why: once a company is struck off the register, it legally ceases to exist. Any property or assets it still owns—and that includes money left in a bank account—automatically passes to the Crown. This is a legal principle known as ‘bona vacantia’ (vacant goods).

Here’s a real-world example:

Imagine ‘Design Project Ltd’ has £500 left in its business account. The director forgets to close it before the company is dissolved. That £500 is no longer accessible to the director; it legally belongs to the Crown. Getting it back involves a complicated, expensive, and long-winded legal process that will cost far more than the original amount.

Always make sure the final balance is zero and you have written confirmation from the bank that the account is officially closed before you submit the DS01 form.

Resolve Any Director’s Loans

Finally, you need to deal with any director’s loans. This is simply money that you’ve either lent to the company or borrowed from it.

- If you lent money to the company: The company must repay you before it’s closed. Since a dormant company has no funds, this loan would typically need to be written off. You must formally document this in a board minute, recording it as a gift to the company to clear the liability from its books.

- If you borrowed money from the company: You must repay it in full. Leaving a director’s loan outstanding means the company still has an asset (the debt owed to it), which will block a strike-off.

Ensuring these loans are properly settled and documented is the final piece of the pre-closure puzzle. Getting this checklist right transforms closing a dormant company from a potential headache into a straightforward administrative conclusion.

Filing the DS01 Form and Notifying Interested Parties

Once you’ve ticked off all the pre-closure checks, it’s time for the main event: formally applying to have your company struck off. This all hinges on one key document – form DS01. While the form itself looks surprisingly simple, getting the details spot on is crucial for a smooth shutdown.

This step takes your closure plans from an internal decision to a public declaration. Think of it as firing the starting pistol for the dissolution process. It triggers a series of legal duties you must follow to the letter, ensuring your application gets accepted without a hitch.

Completing the DS01 Form

The DS01 form, officially titled ‘Striking off application by a company’, is your formal request to Companies House. You can file it online, which is usually quicker, or go the traditional route by post. The form just asks for basic company info – your full company name, registration number – and the signatures of the directors.

The signatures are a critical detail. A majority of the company’s directors must sign the application. If your company has two directors, both need to sign. If you have three, at least two must sign.

Let’s look at a real-world example: ‘London Creative Hub Ltd’ has three directors. Two are in the UK handling the closure, but the third is overseas and hard to reach. As long as the two UK-based directors sign the DS01, the application is perfectly valid and ready to go.

There’s a small, non-refundable filing fee to pay to Companies House. You can check the current fee on the GOV.UK website, but it’s a very modest administrative cost.

It’s worth remembering that when you sign the DS01, you’re making a legal declaration. You are personally confirming that the company has met all the conditions for a strike-off, like having ceased trading for at least three months and having no outstanding debts.

The Legal Duty to Notify Interested Parties

Submitting the DS01 is only half the battle. By law, you must inform all “interested parties” about your application within seven days of sending it to Companies House. This is a non-negotiable legal obligation, and failing to do it is a criminal offence that could land the directors with a fine or even prison time.

This rule exists to give anyone with a legitimate interest in the company a fair chance to object. If they believe they are owed money or have another valid reason, this is their window to speak up.

So, who exactly are these interested parties? The list is very specific:

- Shareholders (Members): Every single one needs to be told.

- Creditors: This includes banks, suppliers, HMRC, and even former landlords. You have to notify them even if you’re certain you’ve settled all accounts.

- Employees: Any past or present employees must be informed.

- Directors Who Didn’t Sign: If a director was part of the majority but didn’t physically sign the form, they must also get a copy.

- Service Providers: Any company that current provides any service under contract to your company.

How to Send the Notification

You can’t just send a quick email. You are required to post a physical copy of the completed DS01 application form to each of these parties at their last known address. This ensures there’s a clear paper trail proving you’ve done your duty.

Actionable Insight: Keep a simple log of who you sent notifications to, the date you posted them, and the address you used. This record could be invaluable if anyone later questions whether you fulfilled your obligations. For directors juggling various compliance tasks, understanding the full scope of these duties is vital. Many of the principles align with those covered in a breakdown of UK company secretary duties and responsibilities, even if your company doesn’t have a formal secretary.

Forgetting this step is one of the quickest ways to have your application blocked. Imagine you used a web hosting supplier two years ago and believe the account is settled. If you don’t send them a notice, but they find an old unpaid invoice for just a few pounds, they have every right to object. Your application would be suspended immediately. It’s always better to be overcautious and notify everyone. This simple bit of communication is your best defence against delays and objections, paving the way for a clean, final closure.

What Happens After You Apply: Timelines and Pitfalls

Once you’ve submitted the DS01 form and sent your letters, the process enters a formal waiting period. This final stretch is mostly hands-off, but it’s where all your careful preparation really pays off. Knowing the official timeline and the potential hiccups that can pop up will help you navigate this last phase without any stress.

Your application kicks off a series of public notifications run by Companies House. This is all about transparency, giving anyone with a genuine interest a last chance to look over your plans to close the company.

The Official Dissolution Timeline

After Companies House accepts your DS01, a very specific timeline begins. The first thing you’ll see is a notice published in the relevant edition of The Gazette, which is the UK’s official public record. For a company registered in England and Wales, that means the London Gazette.

This publication is basically the starting pistol for a two-month objection period. During these two months, any interested party can raise a formal objection to your company being struck off. If nobody objects by the end of this period, Companies House will move on to the final steps.

A second notice is then published in The Gazette, this time confirming that the company has been officially struck off the register. At this point, your company legally ceases to exist. All in all, the entire process from application to final dissolution usually takes about three to four months.

Common Pitfalls That Can Derail Your Application

While the timeline itself is straightforward, a few common problems can pause or even completely stop your application in its tracks. Being aware of these pitfalls is the best way to ensure a smooth journey.

By far, the most frequent issue is someone raising an objection. This formally freezes the strike-off process, and Companies House will write to you to let you know what’s happened.

So, why would someone object?

- An Unpaid Creditor: A supplier might stumble upon an old invoice you completely forgot about.

- HMRC Intervention: If HMRC believes there are any loose ends with your tax affairs, they will almost certainly object.

- Legal Disputes: Someone may have a pending legal claim against the company that needs resolving.

Actionable Insight:The best way to dodge objections is through meticulous preparation. Double-checking that every last liability is settled and every required notification has been sent is your best insurance policy against last-minute delays.

It is important to remember that the companies legal obligations such as record keeping, statutory duties under the Companies Act etc continue to apply right up to the time that the company is finally dissolved. None compliance with such requirements can have serious consequences for both the company and its officers.

Dealing with Unexpected Mail and Objections

What happens if something unexpected crops up during that two-month window? It’s more common than you’d think and needs to be handled correctly and quickly.

Imagine a forgotten supplier sends a final demand letter to your registered office after you’ve already applied. This creates a new liability. Legally, you must withdraw your strike-off application immediately using form DS02. You’d then have to settle that debt before you can restart the whole process.

Another potential headache is mail management. If an important letter arrives at your registered office and you miss it, it could lead to an objection you don’t even know about. This is why some directors choose to use mail forwarding. If you’re worried about missing a crucial notice, you might find our guide on UK business post redirection useful to ensure nothing slips through the cracks.

If an objection is raised, don’t panic. The first step is to get in touch with the objector and understand the problem. For most dormant companies, it’s usually a simple misunderstanding or a small, overlooked bill. Once you’ve sorted it out, the objector can retract their objection, and the dissolution process can get back on track. Getting through these final hurdles successfully is all about being prepared and responsive.

Common Questions About Closing a Dormant Company

Even with the clearest plan, a few niggling questions often pop up when you get down to the finer points of closing a dormant company. Let’s tackle some of the most common queries we hear from directors, giving you straightforward answers for those specific situations you might run into.

Can I Close a Company with an Outstanding Bounce Back Loan?

This is a firm and absolute no. You cannot use the straightforward strike-off process if your company has an outstanding Bounce Back Loan (BBL). A BBL is a serious liability, and trying to dissolve the company without dealing with it can land the directors in hot water.

The government and the banks are actively scrutinising these loans. If you attempt to strike off the company to get out of repaying the debt, it will almost certainly trigger an objection to the closure and could lead to an investigation into your conduct as a director.

If your company has a BBL it can’t repay, you must get professional advice. The only legitimate route is a formal liquidation, where a licensed insolvency practitioner is appointed to wind up the company’s affairs and handle its debts.

What Happens if I Forget to Close the Company Bank Account?

Forgetting this step is a critical mistake with major consequences. The moment a company is struck off the register, it legally ceases to exist. Any assets it still holds—including every penny left in a bank account—automatically pass to the Crown. This is a legal principle known as ‘bona vacantia’ (vacant goods).

Forgetting to close the account means any cash left in it is effectively frozen and handed over to the government. Getting it back is a long, expensive, and complicated legal process that often costs more than the money you’re trying to recover.

Actionable Insight: Before you even think about submitting your DS01 form, make this a non-negotiable item on your final checklist. Transfer every last penny out, make sure the balance is zero, and get written confirmation from the bank that the account is officially closed for good.

How Long Does the Entire Dissolution Process Take?

As long as there are no hiccups, the timeline for closing a dormant company is pretty predictable. From the day your DS01 application is accepted and the notice is published in The Gazette, a statutory two-month objection period kicks in.

During this two-month window, anyone with a legitimate interest (like a creditor) can raise an objection, which will pause the process.

- Best-Case Scenario: If no one objects, the company is usually struck off very soon after the two-month period is up.

- Typical Timeline: Realistically, you should plan for the whole process—from sending the DS01 to final dissolution—to take around three to four months.

This assumes you’ve done all your homework correctly, like filing final accounts and telling everyone who needs to know. Any mistakes or forgotten steps during your preparation will definitely cause delays.

Wading through the final bits of company admin can be tricky, but with the right help, it becomes a simple box-ticking exercise. If you need a hand making sure your company’s filings are all in order or require a professional address service during the closure, Acorn Business Solutions provides the expert, UK-focused support you need. We’ll help you close your dormant company with complete confidence. Find out more at https://acornbusinesssolutions.com.

Related Topics

Professional Indemnity Insurance

Discover what is professional indemnity insurance, why your business needs it, and how it shields you from costly client claims.

What is a company secretary

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

How Do You Redirect Your Mail in the UK?

Moving home? Learn how do you redirect your mail with Royal Mail or private services. A practical guide to costs, setup,

Top accounting courses for small business in the UK (2025)

Discover accounting courses for small business in the UK. Compare top options, pricing, and formats

UK Business Bank Accounts With No credit Checks

Discover UK business bank accounts with no credit checks. This guide explains your options and eligibility

Managing cash flow for small business: Quick tips

Discover managing cash flow for small business with practical steps to forecast, optimize liquidity,